Private credit has grown like an underground river — initially narrow and unnoticed, then gradually widening until it reshapes the entire landscape above it. What began as a niche response to the retreat of traditional banks after the global financial crisis has evolved into one of the most significant forces in modern finance. By 2026, private credit is no longer a peripheral alternative; it is a central artery through which capital flows to businesses, infrastructure and even other financial institutions.

Unlike traditional lending, private credit operates in a realm defined by negotiation rather than standardization. Loans are structured privately, often tailored to the needs of mid-sized or leveraged companies that fall outside the rigid frameworks of banks or public bond markets. This flexibility has made private credit both attractive and dangerous — attractive because it fills gaps left by banks, and dangerous because those gaps often exist for a reason. In this sense, private credit is like water flowing into cracks in a dam: It provides necessary pressure relief, but over time, it may also widen the cracks themselves.

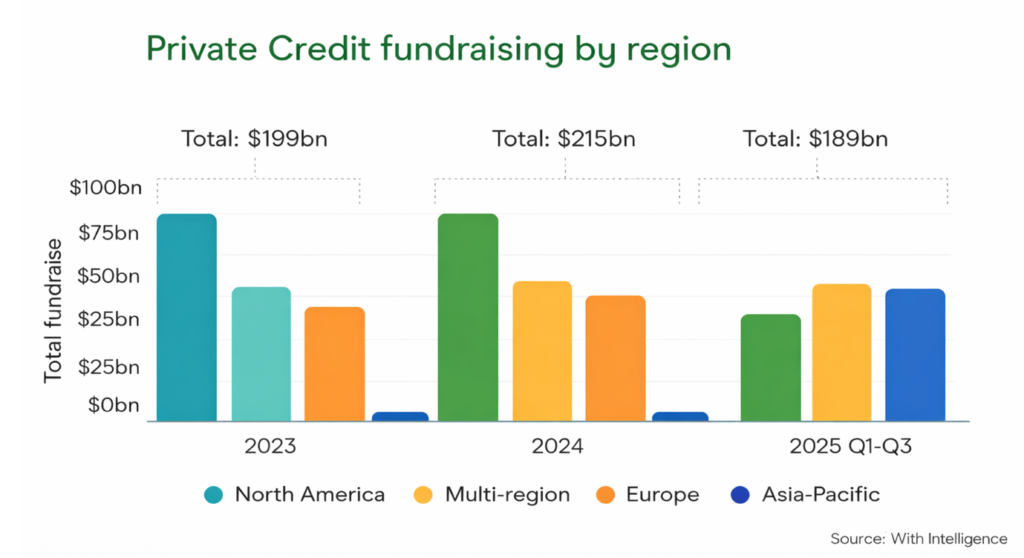

The scale of this transformation is striking. Industry survey-based estimates indicate that the global private credit market has reached approximately $3.5 trillion in assets under management, according to data reported by the Alternative Credit Council in 2025, although the figure depends on broad definitions and survey-based estimates. It rivals major segments of public credit markets and continues to expand, fueled by institutional investors seeking yield in a low-return world and, increasingly, by private wealth channels. What was once an institutional domain dominated by pension funds and endowments is now opening to retail investors through semi-liquid and evergreen structures, fundamentally altering the composition of capital.

Yet this rapid expansion has occurred largely outside traditional regulatory oversight. Unlike banks, private credit funds are not subject to the same capital requirements or supervision. Unlike public bonds, their pricing is not continuously tested by the market. As a result, private credit has developed in a space that is both innovative and opaque — a shadow system that is becoming too large to ignore.

II. Cracks beneath the surface

Despite its outward strength, the private credit market in 2026 shows increasing signs of strain. The surface may appear calm, but beneath it, pressure is building. Borrowers are facing higher interest rates after years of cheap money, and many are struggling to service their debt. The widespread use of payment-in-kind (PIK) interest — a noncash payment method in which borrowers pay interest by issuing additional debt or equity rather than cash, thereby preserving liquidity while increasing the principal through compounding — is a clear signal that cash flows are under stress.

At the same time, the true default rate appears to be higher than headline figures suggest. While commonly cited default rates in private credit often remain around 2–3%, more comprehensive measures indicate significantly higher levels of distress. According to Fitch Ratings, the US private credit default rate reached 5.8% for the trailing 12 months through January 2026, reflecting the highest level since the metric’s inception. Importantly, a large share of these default events is associated with payment deferrals, PIK interest and distressed restructurings rather than outright payment failures. This discrepancy highlights a key issue: Conventional default metrics may understate underlying fragility by excluding softer forms of financial distress.

The situation is further complicated by borrowers’ financial health. Around 40% of private credit borrowers now have negative free cash flow, a sharp increase from previous years. This means that many companies are not generating enough income to cover their expenses, let alone their debt obligations. In a low-interest-rate environment, such companies could survive by refinancing or restructuring. In today’s higher-rate environment, those options are becoming increasingly limited.

These developments suggest that private credit is entering a late-cycle phase, where the risks accumulated during years of easy money begin to surface. It is like a forest that has grown dense and lush after years of favorable weather — beautiful on the surface, but increasingly vulnerable to fire.

III. Liquidity, valuation and the illusion of stability

One of the most significant vulnerabilities in private credit arises from the structural mismatch between the liquidity offered to investors and the underlying illiquidity of the assets. While many funds provide periodic redemption opportunities, these are typically subject to strict caps — often around 5% of assets per period — designed to prevent forced asset sales. In normal conditions, such mechanisms appear sufficient. However, when investor demand for liquidity rises sharply, these constraints become binding, forcing funds to ration withdrawals rather than meet them in full.

Recent developments illustrate how quickly this mismatch can become destabilizing. In several high-profile cases, including funds managed by Blue Owl Capital and Ares Management, redemption requests exceeded allowable limits, resulting in investors receiving only a fraction of their requested capital. In some instances, payouts were reduced to well below one-quarter of requested amounts. Such dynamics resemble a “slow-motion bank run”: Rather than triggering an immediate collapse, liquidity constraints gradually erode investor confidence as expectations of access to capital are revised downward.

This tension is compounded by the valuation framework underpinning private credit. Unlike publicly traded securities, these assets are typically marked using net asset value (NAV), based on internal models or manager estimates rather than observable market prices. While this approach dampens reported volatility and creates the appearance of stability, it also introduces a disconnect between stated valuations and realizable prices under stressed conditions. In effect, valuations become smoother not because risks are lower, but because they are tested less frequently.

The reliance on NAV becomes particularly problematic in structures where funds hold positions in other private credit vehicles. In such cases, valuation can become circular: One fund’s reported NAV is derived from another’s, creating a chain of interdependent assumptions. This recursive valuation process weakens the informational content of prices, as asset values are increasingly anchored in model-based estimates rather than market-clearing transactions.

The combined effect of these features is the emergence of an “illusion of stability.” Reported prices remain steady, volatility appears subdued and performance seems consistent. Yet this apparent resilience is, to a significant extent, an artifact of valuation conventions and liquidity management practices rather than a reflection of underlying economic fundamentals. As long as redemption pressures remain contained and assets are not forced into the market, the system appears robust. However, once these constraints are tested, the gap between reported and realizable values may become evident, revealing vulnerabilities that had previously been obscured.

IV. Structural evolution and the new financial ecosystem

While risks are rising, the private credit market is simultaneously undergoing profound structural transformations that are reshaping its role within the global financial system. One of the most significant developments is geographic diversification. As the US direct lending market becomes increasingly competitive and compressed, institutional investors are reallocating toward Europe, where fragmented market structures and informational inefficiencies create opportunities for higher risk-adjusted returns.

At the same time, new strategies are emerging and scaling rapidly, reflecting a broadening of the private credit ecosystem. Asset-based finance — lending against specific collateral such as receivables, infrastructure or real assets — is gaining prominence and may eventually rival traditional direct lending. Similarly, the expansion of credit secondaries is enhancing market dynamism by providing liquidity solutions for existing portfolios and facilitating balance sheet management among investors.

Another important structural shift is the rise of evergreen funds and other forms of perpetual capital. Unlike traditional closed-end vehicles, these structures allow investors to remain invested indefinitely, offering periodic liquidity rather than fixed exit horizons. While this evolution provides funding stability for managers and supports long-term capital deployment, it also introduces new challenges related to liquidity management, valuation and governance.

Perhaps the most transformative development is the growing role of private wealth. Individual investors, attracted by higher yields in a low-return environment, are increasingly allocating to private credit through semi-liquid vehicles. This influx of capital is altering the composition of the investor base and shifting the balance of power within the market, as asset managers adapt product design, liquidity features and reporting practices to meet the preferences of a more heterogeneous set of investors.

Taken together, these developments suggest that private credit is not a static asset class but a rapidly evolving system of financial intermediation. As I argue, the expansion of private credit is increasingly driven by supply-side dynamics — particularly institutional portfolio reallocation and funding structures — rather than by borrower fundamentals. In this context, systemic risk is not eliminated but reconfigured, shifting from traditional borrower leverage toward vulnerabilities associated with liquidity transformation, interconnectedness and nonbank financial intermediation.

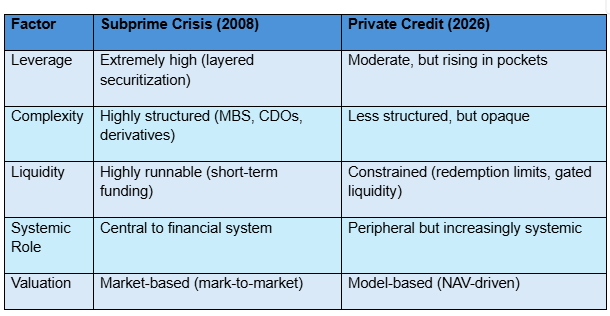

This reconfiguration of risk can be further understood by comparing the structural characteristics of private credit with those of the subprime mortgage market prior to the 2008 financial crisis.

While private credit differs from subprime in important respects — particularly in its lower reliance on short-term funding and reduced run dynamics — its opacity, constrained liquidity and growing interconnectedness suggest that vulnerabilities may emerge in more gradual but less visible ways. Rather than triggering an abrupt systemic collapse, risks in private credit are more likely to accumulate beneath the surface, becoming evident only when liquidity constraints bind or valuations are tested under stress.

In this sense, the private credit market resembles an expanding financial network: It is becoming more complex, more interconnected and more central to the functioning of global finance. This evolution creates new opportunities for capital allocation and diversification, but it also introduces new forms of fragility that are diffuse, less transparent and potentially more difficult for regulators and market participants to detect in real time.

V. Crisis, adjustment or transformation?

The central question facing private credit in 2026 is whether it is heading toward a crisis or simply going through a period of adjustment. Comparisons to the subprime mortgage market are hard to avoid. Both expanded rapidly, operated with limited transparency and became increasingly interconnected. But the differences are just as important.

Private credit today is generally less leveraged and less complex than the structured products that fueled the 2008 crisis. Its investor base is more stable, relying heavily on long-term capital rather than short-term funding. Banks, meanwhile, have relatively limited direct exposure and have shifted much of the risk off their balance sheets through tools such as synthetic risk transfers. Even the parts of the market that offer liquidity to retail investors remain relatively small, despite recent redemption pressures on funds run by firms like BlackRock, Morgan Stanley, Apollo Global Management and Cliffwater.

All of this makes a sudden, system-wide collapse less likely. Private credit has not fueled a single, concentrated bubble in the way that subprime lending did in housing, and most companies still have access to alternative sources of financing. But that doesn’t mean the risks are small — it just means they are different.

The real shift lies in how risk is transmitted. In traditional credit cycles, stress builds through excessive borrowing by companies. In private credit, pressure is more likely to emerge through the financial system itself — through lenders’ balance sheets, funding structures and investor expectations.

That dynamic is becoming increasingly visible in the financing of artificial intelligence. The rapid build-out of data centers, chips and cloud infrastructure has attracted large flows of private capital, often supported by private credit and structured financing arrangements. In some cases, the same firms act as borrowers, investors and counterparties within closely linked networks, raising the risk that capital circulates within the system without being fully anchored in external demand. This creates conditions that resemble earlier episodes of technology-driven exuberance, where expectations run ahead of realized economic returns.

Signs of strain are already visible. Default rates have risen into the mid-single digits, according to Fitch Ratings, and much of that stress is showing up not as outright failures, but as restructurings and delayed payments. At the same time, the features that make the system appear stable — limited liquidity, redemption caps and model-based valuations — can also delay the recognition of problems and stretch them out over time.

This is where external shocks begin to matter. The ongoing tensions involving Iran and the resulting surge in oil prices are already pushing up inflation and weighing on global growth. Even a sustained increase in energy prices can slow economic activity and tighten financial conditions worldwide. In that environment, weaker borrowers — many of whom rely on continued access to credit — become more vulnerable.

Private credit may act as an amplifier of broader economic stress. A slowdown driven by higher energy costs, geopolitical uncertainty or a reassessment of overly optimistic expectations in sectors like artificial intelligence can feed through the system, tightening financing conditions and exposing weaknesses that had been hidden during more benign times.

In many ways, private credit is now being tested for the first time under real strain. It grew rapidly in an era of low interest rates and abundant liquidity, but its resilience in a more challenging environment remains uncertain.

The most likely outcome is not a clean divide between crisis and stability, but a period of adjustment. Some firms will exit, others will adapt and the system will evolve. In the process, private credit will move further into the mainstream of global finance — no longer operating in the shadows, but increasingly shaping how capital flows through the economy.

The question, then, is not whether private credit matters. It already does. The real question is how resilient it will be as its role continues to expand — and whether the financial system around it is prepared for what that expansion brings.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

FO Exclusive: Big Trouble in the US Private Credit Market

In this section of the March 2026 episode of FO Exclusive, Atul Singh and Glenn Carle warn that the $2...

Private Credit Turned Out to Be an Illusion. What’s Next?

The global financial system faces stress as private credit funds struggle with investor withdrawals. BlackRock froze redemptions after massive requests,...

Credit Insecurity in America: Rebuilding Resilience Through Financial Access

Credit access is a critical yet often overlooked dimension of economic inequality in the United States, providing infrastructure that enables...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment