Why do Global South (GS) economies increasingly confront financial tightening, policy paralysis and development divergence despite maintaining stable macroeconomic fundamentals and avoiding overt geopolitical alignment? This question has become central to contemporary debates in the global political economy.

In several episodes over the past decade, emerging market and developing economies (EMDE) sovereign spreads and capital inflows have moved sharply in response to global financial conditions and geopolitical risk, sometimes out of proportion to near-term changes in domestic fundamentals; this has shortened policy horizons and complicated the financing of long-gestation industrial strategies. These patterns are no longer episodic anomalies attributable to idiosyncratic shocks. They reflect a persistent and geographically diffuse condition observable across Latin America, Southeast Asia, the Middle East and Sub-Saharan Africa.

Weaponized uncertainty as a structural condition in the global political economy

Conventional explanations are increasingly insufficient. Trade-centered accounts emphasize tariff exposure or export concentration, yet they cannot explain why economies not directly targeted by trade restrictions experience pronounced volatility. Institutional explanations point to governance quality, credibility or rule of law, but divergence is now evident among countries with comparable institutional indicators and policy frameworks. Sanctions-based frameworks are similarly limited: Many of the most financially constrained states are neither sanctioned nor credibly threatened with formal sanctions.

The puzzle, therefore, is not why punished states suffer, but why unpunished and ostensibly neutral states increasingly do.

Contemporary great-power rivalry has transformed uncertainty itself into a durable instrument of power. Rather than operating primarily through explicit rules, formal coercion or retrospective punishment, geopolitical competition now functions through persistent ambiguity, discretionary enforcement and policy volatility. Together, these elements produce what I term weaponized uncertainty. Under such conditions, uncertainty ceases to be an episodic shock that markets price and absorb. Instead, it becomes a structural feature of the international system — one that reshapes expectations, reallocates risk and disciplines states through financial channels.

The analytical novelty lies in treating uncertainty not as exogenous noise or informational friction, but as an endogenously produced political condition with systematic distributive consequences. During earlier phases of globalization, uncertainty was constrained by institutions that anchored expectations — multilateral trade rules, predictable financial backstops and relatively stable security commitments.

Even where power asymmetries existed, they were mediated through rule-based frameworks that limited discretion. Today, by contrast, major powers increasingly reserve unilateral authority over access to markets, currencies, payment systems, technology platforms and supply chains. Commitments are framed as conditional and reversible; enforcement is selective; escalation thresholds are deliberately opaque.

This shift is explicit in the US’s 2025 National Security Strategy, which frames economic access, technological integration and financial connectivity not as entitlements of system membership but as contingent instruments of national security. Strategic ambiguity is thus not accidental: It preserves flexibility for major powers while systematically shifting adjustment costs onto weaker states.

This shift reflects a broader transformation in global governance away from rule-based coordination toward what professors Henry Farrell and Abraham L. Newman conceptualize as weaponized interdependence, in which control over central nodes of economic networks becomes a source of coercive leverage. Weaponized uncertainty extends this logic. It does not require the active exercise of coercion. Instead, it operates by shaping beliefs about how interdependence might be weaponized under future contingencies. The threat is probabilistic rather than declaratory, anticipatory rather than reactive.

Recent events surrounding Venezuela illustrate this broader shift toward discretionary power and the signaling value of ambiguity in hemispheric competition. Analyses of the US-led capture of Venezuelan President Nicolás Maduro emphasize not only the operational act itself but its geopolitical message — particularly toward China — regarding limits to influence in the Western Hemisphere.

These accounts foreground the revival of “spheres of influence” discourse and the explicit linkage between security actions and economic access, including oil markets, financial channels, regional investment and infrastructure. The analytic point here is not Venezuela per se, but what the episode reveals about the governing logic of a fragmented order: Access is increasingly framed as contingent, revocable and strategically administered.

As Director of International Economics at the Council on Foreign Relations Benn Steil argues, the Maduro episode is best understood not as an idiosyncratic act of regime change, but as part of a broader effort to normalize discretionary assertions of regional dominance in place of universal rules. For the GS, the significance of this shift lies not in the revival of formal doctrines such as the Monroe Doctrine, but in the normalization of spatialized discretion.

When access to markets, finance and security is conditioned on power or alignment rather than rules, uncertainty becomes structural: Markets price political exposure under alternative geopolitical futures. When access to markets, finance and security is conditioned on power or alignment rather than rules, uncertainty becomes structural: Markets price political exposure under alternative geopolitical futures.

The consequences for GS economies are significant.

Sovereign risk is increasingly priced not solely on domestic fundamentals, but on the perceived probability of future exclusion from trade regimes, financial infrastructure or strategic supply chains in plausible escalation scenarios. This shift from expected outcomes to tail risks reshapes financial conditions across countries: Even small increases in perceived exclusion risk can sharply raise risk premia, shorten debt maturities and destabilize exchange rates, particularly in economies dependent on external financing.

Recent episodes show that sovereign risk in emerging and GS economies is increasingly priced on geopolitical tail risks rather than contemporaneous fundamentals: in Russia, spreads and currency weakness rose ahead of the invasion on fears of Society for Worldwide Interbank Financial Telecommunication (SWIFT) exclusion; in Sri Lanka, external debt build-up and vulnerability were reflected in rising risk premia and tightening financing constraints well before default.

Market volatility thus reflects anticipated geopolitical vulnerability rather than contemporaneous policy failure.

Crucially, this repricing operates ex ante. Financial markets act on beliefs about future alignment and exposure before sanctions are imposed or alliances formalized, eroding policy space in advance of any concrete policy choice. Weaponized uncertainty, therefore, disciplines states preemptively, generating a chilling effect on development strategies that rely on stable financing and long planning horizons. The GS’s predicament is thus structural rather than institutional — a position within a financialized geopolitical order in which uncertainty itself functions as a sorting mechanism.

The global south trilemma and the financial enforcement of geopolitical order

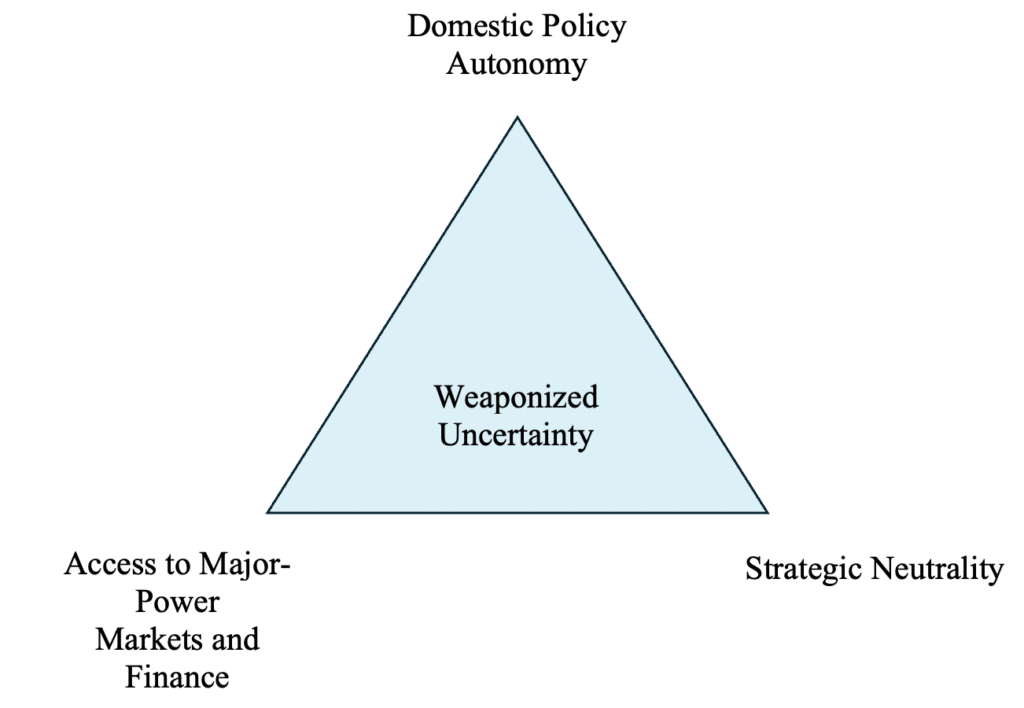

Under conditions of weaponized uncertainty, GS states confront a trilemma defined by three objectives that were once jointly attainable but have become increasingly incompatible:

- Sustained access to major-power markets, currencies and financial systems

- Strategic neutrality or hedging amid great-power rivalry

- Domestic policy autonomy, including industrial policy and long-term development planning

In earlier phases of globalization, these objectives could be mutually reinforcing. States diversified trade relationships, avoided formal alignment and pursued domestic development strategies within a broadly predictable institutional environment. Neutrality often functioned as a buffer, insulating countries from geopolitical shocks while allowing them to arbitrate between competing blocs.

Weaponized uncertainty fundamentally alters this equilibrium. As access to economic infrastructure becomes increasingly discretionary, neutrality ceases to signal insulation and instead signals exposure. From the perspective of financial markets, a neutral state lacks guaranteed protection from exclusion by any major power. In an environment where escalation pathways are unclear and enforcement is selective, neutrality becomes difficult to price — and therefore risky.

This logic helps explain why states attempting to hedge between major powers often experience greater volatility than clearly aligned states, and why policy autonomy erodes not after failure but in anticipation of potential geopolitical misalignment.

Inspired by Turkish economist Dani Rodrik’s globalization trilemma, I propose an original framework tailored to a financialized geopolitical order, in which the binding trade-offs faced by GS states arise not from democratic constraints but from the interaction between market access, strategic alignment and policy autonomy under conditions of weaponized uncertainty. Figure 1 illustrates the trilemma faced by GS states between (i) access to major-power markets and financial systems, (ii) strategic neutrality in great-power rivalry and (iii) domestic policy autonomy.

Under conditions of weaponized uncertainty, the interior of the trilemma becomes binding: Combinations of objectives that were previously feasible under rule-based globalization generate heightened financial volatility and policy constraint. Uncertainty operates as a disciplining mechanism by raising the perceived tail risk of exclusion, thereby tightening the trade-offs among the three objectives even in the absence of domestic policy failure.

Financial markets play a central governance role in enforcing this trilemma through three interrelated mechanisms.

First, markets reprice sovereign risk around worst-case scenarios rather than baseline macroeconomic trajectories. In an environment characterized by discretionary power, investors need not believe that exclusion will occur with certainty. It is sufficient to assign a non-trivial probability to an exclusion pathway under escalation. As Knightian uncertainty replaces measurable risk, the pricing kernel shifts toward adverse tails.

Second, markets shorten investment horizons by privileging liquidity over commitment. Even when fundamentals remain stable, the perceived distribution of outcomes becomes fatter-tailed when market access is contingent on geopolitical classification. Shorter horizons translate into higher rollover risk, greater sensitivity to global financial conditions and a systematic bias against long-gestation projects — precisely those required for industrial upgrading and structural transformation.

Third, markets induce preemptive adjustment by governments. Rising spreads, exchange-rate volatility and refinancing constraints incentivize fiscal and monetary compression before any controversial policy is enacted. The result is rational policy paralysis. Governments avoid actions that might trigger or accelerate geopolitical reclassification, particularly in sectors deemed sensitive: dual-use technologies, strategic minerals, logistics nodes and digital infrastructure.

The unifying mechanism is reclassification. Under weaponized uncertainty, states are continuously and probabilistically sorted into geopolitical categories — ally, transactional partner, neutral — with each category carrying distinct expectations about future access and protection. Unlike formal alliance systems, this classification is neither codified nor transparent. It emerges from the interaction of investor beliefs, policy signals and strategic narratives. Yet its consequences are concrete and immediate.

Governing fragmentation: safe harbors, selection risk and the limits of institutional design

If the primary constraint on the GS policy space arises not from weak domestic capacity but from how markets form expectations under weaponized uncertainty, then conventional policy prescriptions — credibility-building, institutional reform or macroeconomic adjustment — are no longer sufficient.

These approaches assume that markets discipline governments mainly on the basis of observable performance, policy coherence and institutional quality. Under weaponized uncertainty, however, markets discipline states according to their anticipated vulnerability to future geopolitical reclassification. What matters most is not what governments are doing today, but what markets believe could happen to them under plausible escalation scenarios.

In Knightian terms, the binding constraint is no longer calculable risk but fundamental uncertainty. Because the structure of the international system is contingent and discretionary, investors cannot reliably assign probabilities to future outcomes. When expectations about future access to markets, financial infrastructure or security arrangements cannot be stabilized, investors overweight catastrophic tail events.

In such environments, improvements in macroeconomic fundamentals or policy frameworks do little to restore confidence, because the dominant concern is not gradual underperformance but the possibility of abrupt and discontinuous exclusion. Addressing this problem, therefore, requires an ex ante intervention that operates directly on expectations by placing credible bounds on worst-case outcomes. This is the motivation behind the proposed GS Safe Harbor Provision (GS–SHP).

GS–SHP should be understood as a cooperative effort between G7 economies and GS states aimed at governing fragmentation before it hardens into permanent division. It does not seek to restore the earlier model of universal, rule-based globalization, nor does it attempt to eliminate great-power rivalry. Instead, it treats rivalry as a durable structural condition and asks whether cooperation can still operate within it to stabilize expectations and preserve policy space. Its central innovation lies in reframing neutrality from a purely diplomatic posture into a contractible institutional status embedded within existing global governance arrangements.

Under GS–SHP, participating GS states would accept a limited and verifiable set of commitments, including transparency standards, reporting obligations and agreed rules governing engagement in geopolitically sensitive sectors. In exchange, G7 economies and other systemically central states would provide pre-committed, conditional protections against abrupt exclusion from key financial and trade infrastructures.

These protections would not be unconditional or permanent. Their stabilizing effect derives not from scale, but from credibility. Even partial and time-bound guarantees can meaningfully reshape market expectations if they convincingly limit catastrophic scenarios and reduce the perceived probability of sudden regime shifts.

Seen in this light, GS–SHP functions less as a transfer mechanism and more as a joint expectation-stabilization framework. For GS economies, it mitigates the anticipatory tightening of financial conditions that discourages long-term investment and industrial policy. For G7 economies, it reduces systemic risks associated with volatile capital flows, supply-chain disruptions, migration pressures and geopolitical spillovers.

More fundamentally, GS–SHP reflects a shift in how economically relevant knowledge is produced and governed. Under weaponized uncertainty, neither markets nor policymakers operate with stable probability distributions or shared models of the future. Behavior is instead guided by beliefs about possible regime breaks, reclassification events and exclusion pathways that cannot be inferred from past data or current performance. In this setting, effective governance does not rest on improving information about fundamentals, but on shaping the range of futures that markets consider plausible. GS–SHP therefore operates as an epistemic intervention: It does not predict outcomes but bounds expectations by redefining which catastrophic scenarios are institutionally credible.

The economic logic follows directly.

Weaponized uncertainty increases the sensitivity of risk premia to geopolitical signals. When uncertainty is unbounded, even minor diplomatic or strategic shifts generate outsized financial reactions, as markets interpret them as potential regime breaks rather than marginal disturbances. GS–SHP reduces this sensitivity by transforming open-ended uncertainty into bounded uncertainty. Shocks are no longer interpreted as triggers for wholesale reclassification, but as deviations within a known and governed institutional range. This lengthens investment horizons, stabilizes access to long-term finance and prevents the preemptive contraction of policy space that characterizes financial discipline under uncertainty.

At the same time, GS–SHP cannot eliminate underlying structural tensions. Any cooperative framework that differentiates between participating and non-participating states necessarily introduces selection risk. Exclusion may itself function as a negative signal, reinforcing the very reclassification dynamics GS–SHP seeks to mitigate. Moreover, eligibility criteria — however technical they appear — will reflect the strategic priorities of dominant states. As British political theorist Susan Strange emphasized, structural power lies in the ability to define the terms of access, credibility and inclusion. Cooperation, therefore, operates within existing power asymmetries rather than outside them.

These tensions point to a broader conclusion. GS–SHP is not a comprehensive solution, but a second-best response to a world in which universal rules no longer anchor expectations. Development divergence in the GS increasingly reflects selection dynamics rather than policy failure. States are sorted less by performance than by how markets and major powers anticipate their future positioning under hypothetical escalation scenarios. Classification itself becomes a central mechanism of governance, operating through financial channels rather than formal legal mandates.

Recognizing this shift requires treating uncertainty not as a residual imperfection to be minimized, but as a governing technology that shapes incentives, reallocates risk and constrains which development paths remain economically viable.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

Money, Power and Policy in an Unequal Monetary Order

Foundations of Money and Banking in India by Ankur Bhatnagar and C. Saratchand delves deep into how global financial power...

Guarding the Gates of the Global Fortress: Great Power Rivalry at Global Strategic Chokepoints

Contemporary great power competition is shifting toward strategic “gateways” of the international system — regions where geopolitical influence, economic infrastructure...

Lines of Power: Resilience Defines the US and China’s Futures

US President Donald Trump’s latest attempt to balance confrontation and conciliation with Beijing reveals the evolution of US–China relations into...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment