Fertilizer rarely commands attention in moments of crisis. Oil shocks dominate headlines, financial markets react instantly to geopolitical tensions, and policymakers mobilize in response to inflation and currency stability. Yet beneath these visible systems lies a quieter foundation that sustains something far more fundamental: the global food supply. If oil is the bloodstream of the global economy, fertilizer is its metabolism — the process that converts energy into life. Without it, modern agriculture would not simply slow; it would contract sharply, reshaping the limits of human survival.

The invisible backbone of the global economy

The scale of dependence is striking. Approximately half of global food production relies on synthetic fertilizers, particularly nitrogen-based inputs such as ammonia and urea. This dependency is structural rather than optional. Fertilizer enables soils to exceed their natural fertility limits, supporting yields that sustain a population of more than eight billion people. In its absence, agricultural output would fall dramatically, not gradually, because modern crop systems are calibrated around high-input, high-yield conditions.

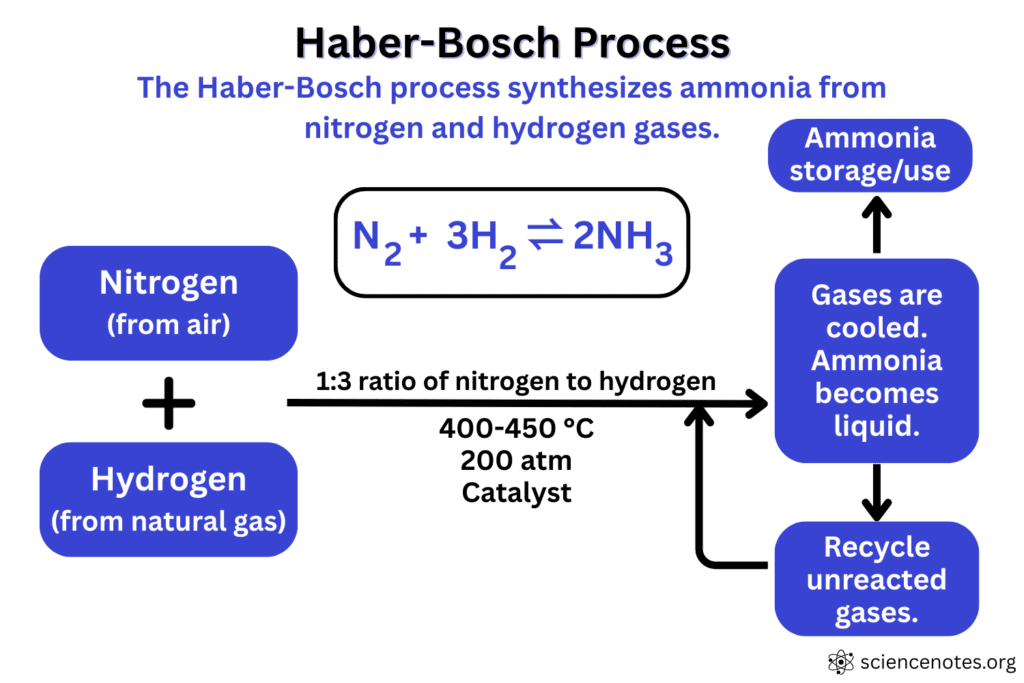

This dependence is further intensified by fertilizer’s deep integration with energy markets. Nitrogen fertilizers are produced through the Haber-Bosch process, which relies heavily on natural gas as both a feedstock and an energy source. As a result, fertilizer prices track energy prices closely. When natural gas prices rise — as they did sharply during recent geopolitical disruptions — fertilizer production costs increase almost immediately. Phosphate fertilizers, meanwhile, depend on sulfur, a byproduct of oil refining, reinforcing the linkage between energy systems and agricultural inputs.

This dual dependency creates a structural vulnerability. Fertilizer is designed to stabilize food production, yet its own supply chain is highly sensitive to shocks. When energy markets tighten or trade routes become uncertain, fertilizer availability and affordability deteriorate rapidly. Unlike other inputs, this deterioration cannot be easily absorbed or delayed.

Recent market behavior illustrates this fragility. During geopolitical tensions in 2026, fertilizer prices rose sharply within weeks. Urea prices increased by roughly 50% in several markets, while farmers reported cost increases of $100 to $300 per ton in Virginia. These movements were not driven by fundamental production shortages but by uncertainty surrounding supply routes and trade disruptions. The system did not collapse — but it became constrained. And in a system with minimal slack, constraint alone is enough to trigger cascading effects.

Fertilizer can be understood through a simple but powerful metaphor: it is the oxygen of agriculture. Oxygen is rarely noticed when it is abundant, yet even small reductions can impair biological function. Similarly, fertilizer is largely invisible in the final food product, but its absence—or even partial reduction—can significantly affect crop yields. The system does not fail immediately, but it weakens, gradually and cumulatively, until its limits are exposed.

The chokepoint that feeds the world

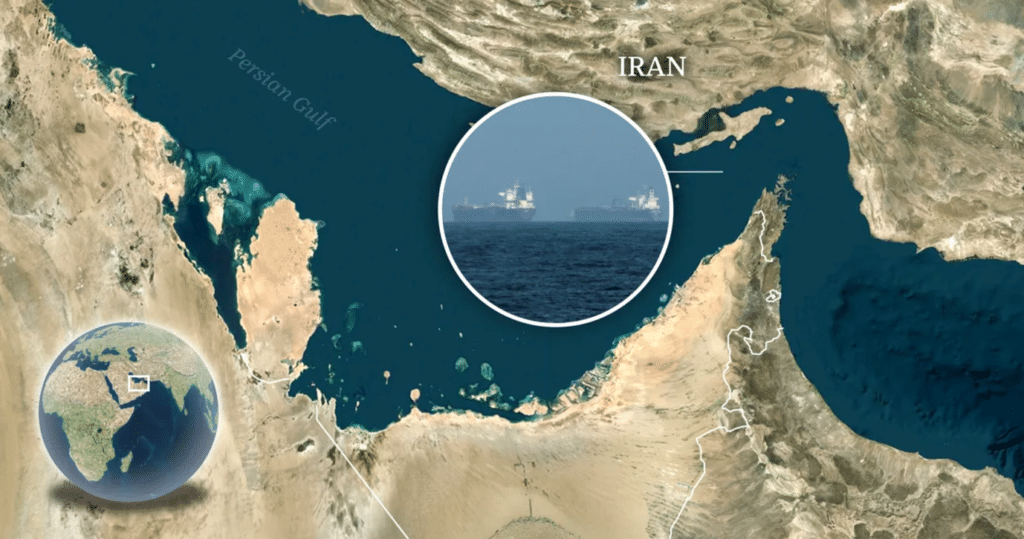

The vulnerability of fertilizer supply is most clearly revealed at a single geographic point: the Strait of Hormuz. Known primarily as a critical artery for global oil shipments, the Strait is equally essential for fertilizer markets, though this fact receives far less attention. A substantial share of global fertilizer exports originates in the Persian Gulf and must pass through this narrow waterway.

The concentration of supply is significant. Countries in the region account for more than 30% of global urea production and a notable share of ammonia and sulfur exports. More broadly, an estimated 30% of global fertilizer trade transits the Strait. This creates a structural bottleneck in the global agricultural system: A localized disruption has the potential to produce global consequences.

What makes this chokepoint particularly dangerous is the absence of viable substitutes. Unlike oil, which can sometimes be rerouted through pipelines or supported by strategic reserves, fertilizer supply chains are less flexible. Production facilities are geographically concentrated, tied to natural gas reserves or mineral deposits, and cannot be easily relocated or expanded in the short term. Transportation networks are similarly constrained, with limited alternative routes available.

The lack of strategic reserves further amplifies this vulnerability. While many countries maintain oil stockpiles to buffer against supply shocks, fertilizer markets lack comparable mechanisms. There is no global system of reserves that can be released in times of disruption. Instead, shocks are transmitted directly into prices and availability, leaving farmers and consumers exposed.

This structural design reflects a broader trade-off between efficiency and resilience. Over decades, global fertilizer production has become increasingly concentrated in regions with cost advantages, optimizing for efficiency under stable conditions. However, this concentration has reduced redundancy. When a critical node such as the Strait of Hormuz becomes unstable, the entire system is affected.

The implications extend beyond logistics. The Strait is not merely a transit point; it is a critical junction linking energy, chemicals and agriculture. It connects natural gas extraction to ammonia production, oil refining to sulfur supply and fertilizer manufacturing to global food systems. Disruption at this node does not just affect one commodity — it affects an entire chain of interdependent processes.

Simulation insight: from fertilizer shock to food inflation

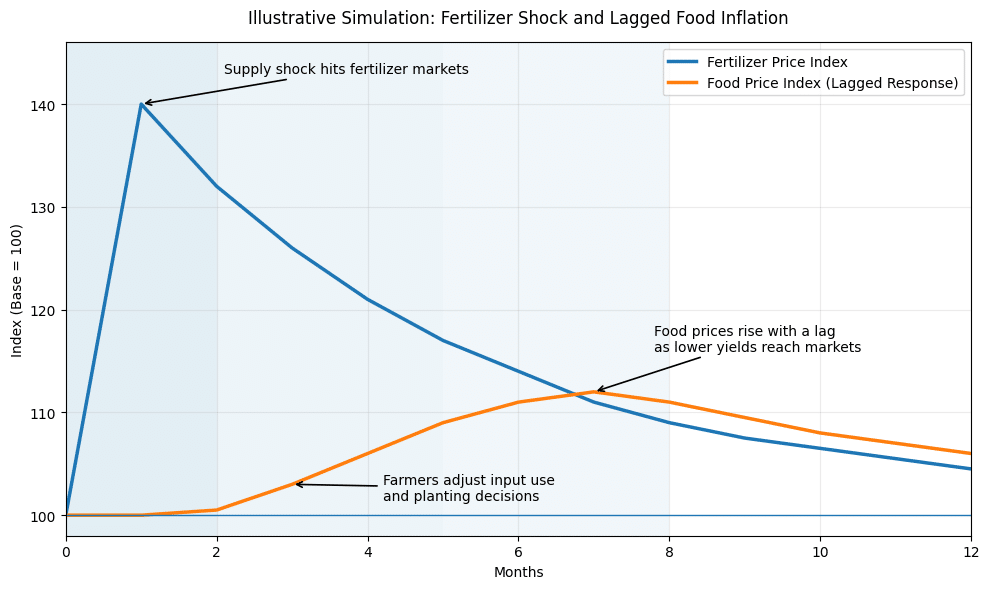

Understanding the broader impact of fertilizer disruptions requires moving beyond static analysis and considering dynamic interactions over time. Fertilizer markets do not operate in isolation; they are part of a lagged system in which cause and effect are separated by months.

A simplified simulation of recent conditions reveals a plausible pattern. When fertilizer prices rise sharply — by roughly 20% to 40% or more — the immediate effect is likely to appear first in farmer behavior rather than retail food prices. Farmers may reduce fertilizer application, delay purchases or shift acreage toward less nutrient-intensive crops. These are rational responses to cost pressure, but their consequences appear with a lag. Food prices may remain relatively stable initially because of inventories, forward contracts and ongoing production cycles. After several months, however, reduced fertilizer use and higher production costs can contribute to higher food prices. In the simulation, this delayed food-price response is smaller than the fertilizer shock — about 5% to 10% — but more persistent.

| A simplified simulation of recent fertilizer shocks reveals a consistent and empirically supported pattern. When fertilizer prices increase sharply — around 20–40% or more — the immediate effect is observed in farmer behavior rather than food prices. Farmers respond within weeks by reducing application rates, delaying purchases or shifting toward less fertilizer-intensive crops. Food prices initially remain stable due to inventories and production lags, but begin to rise after several months, consistent with observed farm-to-retail transmission delays of 1–6 months. The resulting food price increase is smaller in magnitude — typically in the range of 5–10% — but more persistent, reflecting partial pass-through and ongoing production cost pressures. |

This lag structure is not hypothetical. It is supported by empirical evidence. During the 2007–2008 global food crisis, fertilizer price spikes preceded food inflation by several months. A similar pattern was observed following the disruptions associated with the 2022 war in Ukraine. In both cases, the transmission mechanism followed a predictable sequence: input shock, behavioral adjustment, output reduction and price increase.

The key feature of this system is its nonlinearity. Small increases in fertilizer prices may lead to modest adjustments, but beyond a certain threshold, farmer responses become more pronounced. When application rates fall below optimal levels, crop yields decline sharply rather than gradually. This introduces a tipping-point dynamic, in which relatively small shocks can produce disproportionately large outcomes.

This dynamic also explains why fertilizer markets serve as an early warning indicator for food inflation. When fertilizer prices rise sharply and persistently, they signal future constraints in agricultural production. The lag between input costs and output prices creates a window in which the underlying risk is not yet visible in consumer markets.

Based on current conditions, the evidence suggests that even a moderate disruption lasting a single planting season could produce measurable effects on global food prices. Historical relationships between fertilizer costs, energy prices and food inflation indicate that increases in the range of 5% to 10% are plausible. While such increases may appear modest, they can have significant consequences for food security, particularly in regions where households spend a large share of their income on food.

From soil to strategy: fertilizer and global stability

The implications of fertilizer disruptions extend far beyond agriculture into the realm of geopolitics. As food security becomes increasingly linked to national stability, control over fertilizer supply chains is emerging as a form of strategic power. Countries that produce and export fertilizers gain leverage over those that depend on imports, reshaping economic and political relationships.

Recent developments suggest that this dynamic is already taking shape. During periods of disruption, major exporters have strengthened their influence as alternative suppliers, while import-dependent countries have faced heightened vulnerability. Trade flows have, in some cases, become more selective, reflecting geopolitical alignments rather than purely market-based decisions.

This pattern mirrors dynamics observed in energy markets, but with potentially greater consequences. Energy shortages disrupt economic activity, but food shortages can destabilize societies. This elevates fertilizer from a commodity to a strategic asset — one that influences not only markets but also political outcomes.

Looking ahead, several structural trends are likely to shape the future of fertilizer systems. Geopolitical risk is expected to remain elevated, particularly around key trade routes such as the Strait of Hormuz. At the same time, the energy transition may gradually reshape fertilizer production, with investments in green ammonia offering a potential alternative to natural gas-based processes. However, these technologies are still developing and will require significant time and capital to scale.

Agricultural practices may also evolve. Advances in precision farming and soil management could improve fertilizer efficiency, reducing the amount required per unit of output. Yet these innovations are unevenly distributed and unlikely to fully offset supply risks in the near term.

Taken together, these trends point to a system that is becoming more complex, more interconnected and more exposed to disruption. The fertilizer market, once considered stable and predictable, is increasingly shaped by geopolitical forces and structural constraints.

The broader lesson is that global stability depends on systems that are often overlooked. Fertilizer operates quietly, embedded within the global economy, until a disruption reveals its importance. The current tensions surrounding the Strait of Hormuz demonstrate how a single chokepoint can influence not only energy markets but also the availability and affordability of food worldwide.

If oil is the bloodstream of the global economy, fertilizer is its metabolism. Disrupt that process, and the system does not fail immediately — but it weakens, gradually and cumulatively. The next global crisis may not begin with a financial collapse or an energy embargo. It may begin in the soil — with nutrients that fail to arrive, crops that fail to grow and a system that, despite its efficiency, proves less resilient than assumed.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

FO Exclusive: The Dangerous Implications of the New US/Israel–Iran War

In this section of the March 2026 episode of FO Exclusive, Atul Singh and Glenn Carle highlight how Iran’s decentralized...

The World Now Needs Green Trade, Not Free Trade

Corporations are using trade and investment treaties to handcuff global and national efforts to save the planet. That must stop.

The War in Ukraine Threatens Global Food Security

Acute food shortages caused by the war in Ukraine can be absorbed, albeit at higher prices.

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Deal Under Pressure: What India Really Gains from the Trade Agreement with the US

The India-US trade deal only offers modest tariff relief and limited competitive advantages over regional rivals. Furthermore, any benefits arising...

Monetizing Carbon Markets Now: The Results India Needs

India’s farmers produce a sizable chunk of the country’s carbon dioxide (CO2) emissions, and if we are to slow climate...

Big Agribusiness: A Look at Brazil’s Disastrous Rural Feudalism

Agribusiness has made Brazil the world’s largest net exporter. Due to historic property laws, however, land ownership remains a major...

Comment