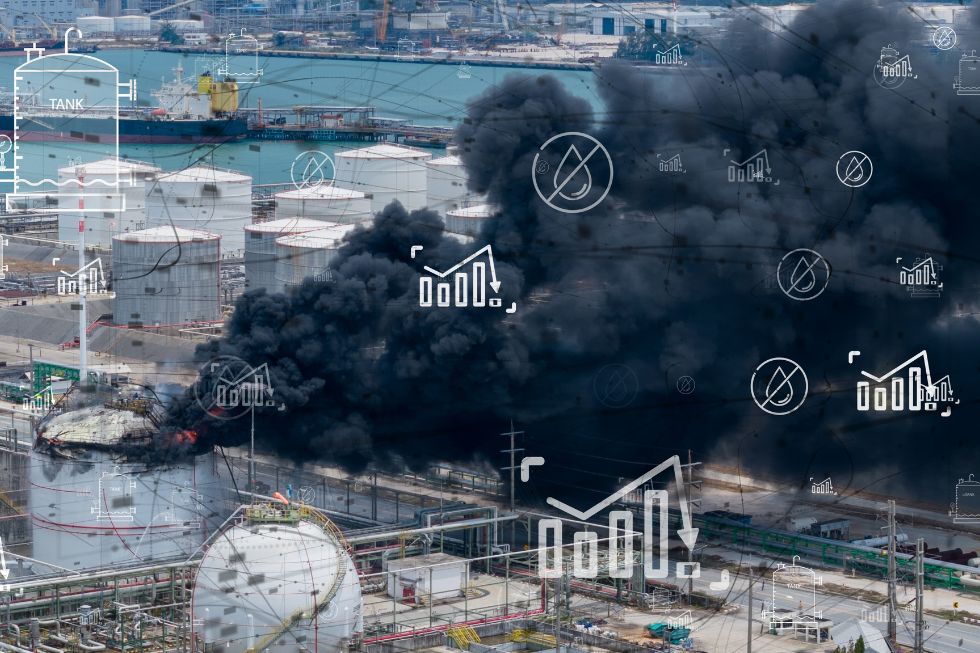

Since the beginning of the US-Israeli attacks on Iran, the Gulf states have been the target of Iranian missiles and drones. For instance, the Kuwaiti Mina Al Ahmedi refinery was struck multiple times throughout the war, and QatarEnergy’s export capacity was reduced by 17% following strikes on Ras Laffan, one of the world’s largest liquefied natural gas (LNG) facilities. The 17% reduction in Qatari LNG exports will last up to five years until full repairs are completed and will cause around $20 billion in annual revenue losses. Amazon data centers were attacked in the United Arab Emirates (UAE) and Bahrain more than once. Residential and civilian facilities, such as power and water desalination plants, were struck by Iran. The Gulf Cooperation Council (GCC) was on the defensive, resulting in a near-total shutdown. Their airspace got closed, and expats were either evacuated or stranded in fear. The halt ended partially; however, the ramifications will linger on for a long time to come, and the toll will be quite heavier than they have already paid.

Economic toll

Unlike Iran, the other Middle Eastern states, especially the six members of the GCC, have strengthened their economic ties with the West. One major example of such economic ties is the one between the EU and the GCC. The 1989 Cooperation Agreement has resulted in over $170 billion in exports and imports between the two sides in 2023.

Over the past five decades, these countries have also worked hard to attract foreign investors, entrepreneurs, and even wealthy individuals seeking to invest in luxury real estate and opulent lifestyles. To name a few examples of such steps, Dubai launched a five-year multiple-entry visa for business trips in 2021, and the UAE began offering five-year residency and renewable 10-year visas to those who own real estate in the UAE valued at $5 million and $10 million, respectively. To attract foreign capital, both Bahrain and Oman have introduced Golden Residency programs that grant wealthy foreigners, including their families, long-term residencies of ten years or longer.

States such as the UAE and Qatar have become reliable hubs for travelers reaching their destinations globally. In 2023, an 18.25% share of the UAE’s GDP was accumulated through aviation. In practice, this means $92 billion in revenue and 992,000 jobs. It is a similar trajectory for Qatar. In 2025, only Qatar Airways Group reported a 28% profit increase over the previous year, surpassing $2 billion. Qatar’s tourism revenue surpassed $10 billion, up 25% from 2023.

Saudi Arabia is another Middle Eastern power with considerable financial clout. Its economic reform for the post-oil Kingdom, known as Vision 2030, aims to improve its biotechnology sector to become not only self-sufficient but also an exporter and global hub for biotechnology. Within this project, other strategies include expanding the mining sector with a focus on minerals, and even the gaming and Esports sector to host international tournaments, as well as attracting foreign companies to Saudi Arabia. The program is reliant on the non-hydrocarbon sector, comprising foundational pillars namely construction, tourism and tech, which are integral to Saudi Arabia’s economic growth, as the World Bank report states, “the non-oil economy’s share of GDP grew from 60 percent in 2015 to 68 percent by 2024”.

With the risks of collapsed tourism, damaged energy infrastructure and logistics disruptions growing manifold, the Gulf countries face an imminent crisis. Amid the worsening security crisis in the region, all of these countries face a heavy blow, with the looming threat of economic devastation, as they remain heavily dependent on such critical sectors to attract foreign investment and capital while diversifying away from oil exports. Their economic leverage rests on regional stability, which has been put under immense strain due to the volatile situation.

More alarming is the emerging scenario in which large companies tend to act quickly to secure their assets and withdraw from a conflict zone; however, their return is a slow, cautious process. Consequently, if the war results in the departure of some foreign companies from the region within a few weeks, their return may take months or years, which would be detrimental to the economies of the GCC in the long term.

Ironically, Iran will not face such a risk, as the Islamic Republic has not been a destination for international firms due to sanctions and an inadequate environment that has not been conducive to foreign investment.

Damaged reputation

Over the past few decades, the Gulf countries have built a reputation as a safe destination. This feature has attracted not only investors and foreign companies but also pensioners and those fleeing high taxation in their home countries. As their reputation is now tarnished by the escalating conflict, it will take a long time to rebuild it and recover from the damage inflicted. During the early stages of the war, Iran hit back hard. Missiles and drones were fired at numerous targets, including airports, residential buildings and industrial complexes.

One small example is the UAE. It is home to around 240,000 British expats. The US–Israel–Iran war has distressed the majority of expats living across the region. It has gone as far as being labeled by some Western news outlets, such as tabloid Daily Mail, as “‘Dubai Is Finished’: Expats say they will leave and never come back as tax-free dream is shattered by war and officials begin prosecuting people for posting videos of missiles.”

Worthy US alliance?

Except for Iran and Yemen, the US is in some sort of alliance with all states in the region. The closest allies are Israel, followed by Saudi Arabia, the UAE, Qatar, Jordan and others. Israel, for instance, has received $330 billion in aid, both military and civil, from the US since its foundation.

The alliance between the Gulf states and the US dates back to the 1940s, when, for instance, US President Franklin D. Roosevelt met with Abdul Aziz Al Saud aboard USS Quincy in 1945. The result was access to Saudi oil for security assurance to the Kingdom. And other Gulf states followed suit and went into an alliance with the US.

Fast forward to 2026, although the Gulf countries do not receive US military aid on the same scale as Israel and Egypt, their arms deals with the US are among the largest. Between 1950 and 2024, Saudi Arabia, Qatar, Kuwait and the UAE have purchased $182 billion, $40 billion, $35 billion and $34 billion, respectively. These massive purchases have certainly helped these countries defend themselves against Iranian drones and missiles; however, the cost of munitions for them is considerably higher than for Iran, as a Shahed-136 drone costs under $50,000, compared with, say, Patriot interceptor missiles that cost $4 million per shot. The ineffectiveness of US military equipment to deter attacks, coupled with US’ waning commitment to uphold its allies’ defense under its security umbrella in the region, propels the Gulf countries to recalibrate their security ties with the US.

After all, it was never their war to begin with, yet they face dire consequences simply for allying with the US (which now appears more to be a grave liability). Since the beginning of the war, Tehran has justified its attacks on Iran’s neighbors by claiming that any location in the region hosting a US military presence is a legitimate target. However, most of the missiles and drones thrown at the Gulf states were not precisely aimed at the American bases, either deliberately or due to a lack of precision, as it has been reported that the Circular Error Probable of Iranian missiles is between 20 and 500 meters. This makes it even harder for states such as the UAE to convince foreigners to stay or even consider returning, once the war is over. Expats, especially those who are attracted by luxury and 0% income tax rate, will hardly be willing to live in a place where even a one percent chance of missile penetration exists, should another round of conflict emerge.

Post-war scenarios

While efforts were recently made to broker a peace deal between the US and Iran, with Pakistan acting as a primary mediator, the talks in Islamabad stalled; however, reports are now surfacing that the conflicting parties are expected to re-engage in negotiations soon.

Regardless, for the Gulf countries, there are mainly two outcomes as of now. The first prediction is that the Iranian regime will be toppled and a new Iran will emerge. In this case, the Gulf states can simply claim that the old threat no longer exists. Hence, it will be relatively easier to convince expats and companies that departed in haste to return. And the Gulf states would emerge shaken but ultimately “victorious”, and their alliance with the US would be seen as worthwhile. Their domestic publics would also be less likely to question the rulers’ strategies and policies. However, this scenario appears very unlikely, given Iran’s position in surviving the war and transitioning to a ceasefire and negotiations, as well as the US stance shifting toward achieving a mere exit strategy.

A second scenario, which is the most likely one to consider, is that the Iranian regime survives the war, in which case the main losers will be the Gulf countries. Iran, the US and Israel will all claim victory and, to an extent, those claims will be correct. The leaders of these three countries will be able to convince their publics that they have achieved their objectives, at least among those who support their governments’ policies. The new Supreme Leader, whether it is still Ayatollah Mojtaba Khamenei or a successor in case he is also killed, will claim that they have defeated the US plan to overthrow the regime, and the IRGC, Basij and regime supporters across all strata will buy it. President Trump will tell his MAGA supporters that he has “obliterated” the threat of a ballistic and nuclear Iran. Prime Minister Netanyahu will tell Israelis, mainly his supporters, that Iran’s capability to attack Israel is diminished.

However, for regional countries such as the UAE, there won’t be a victory narrative to pursue. They will not be able to convince their constituencies by claiming victory, as they have, at best, been defending themselves in a war that was not theirs. The public will be anxious about what the alliance with the US (and in the case of the UAE with Israel) will bring next. The Gulf states will face criticism from their people regarding the alliance with the US and any ties to the state of Israel. History bears witness to this, as public perception in Gulf states has often diverged from government narratives, and state decisions have not sat well with the public.

The defiance was most noticeable in relation to the alliance between the US and Gulf state leaders, which does not always align with how the Arab public perceives the US and Israel. During the 12-day war between Israel and Iran, a Jordanian Cafe offered reservations to customers who would like to enjoy their meals while watching Iranian missiles roaring towards Israel. A similar case happened during the Gulf War. On January 18, 1991, Saddam Hussein’s Iraq launched missile attacks on Israel. In his book, The Achilles Trap, Steve Coll writes that five Iraqi Scud missiles hit Tel Aviv and Haifa while Saudi officers and American counterparts were in the coordination center, C3IC, observing the attacks. The Americans were shocked when they saw the Saudi officers cheering the Iraqi strike with Allahu Akbar.

Now, while the times may differ, similar sentiments persist. Gulf states have to tactfully handle public opinion while simultaneously preventing their economies from falling into the doldrums. Henceforth, the path for the Gulf states is certainly fraught with difficulties on multiple fronts.

In the end, therefore, it is not the US that loses investors and entrepreneurs, nor is it Israel, which is a startup country with the most powerful military in the region. Iran will not suffer from the mistrust of foreign investors either, as the country has few or no foreign investors, especially Western ones, due to sanctions and an unfriendly environment for foreigners. Tehran has little involvement in the international trade community to worry about losing it. What Iran has never had will not be a loss to Tehran in the post-war period. The real costs will be borne by the Gulf states.

[Zahra Zaman edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

The Iran War Is a Reminder: Decarbonize Fast, But Do Not Gamble with Energy Security

The Iran war has disrupted global energy markets by targeting key infrastructure and closing the Strait of Hormuz, a vital...

The Disruptive Iran War, Limits of Western Power and Moral Costs of Grotesque Imperialist Wars

Western imperialism persists through economic sanctions, military interventions and control over global resources, as seen in Venezuela and Iran. Nations...

The Gulf Confronts an Ugly Truth About Aligning With America

Iran’s attacks on bases across the Gulf, including the United Arab Emirates, Qatar, Bahrain, Saudi Arabia and Oman, have shattered...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Sudan’s Crisis Worsens Amid Escalating War and Fading International Support

Sudanese military leaders, foreign governments and aid agencies confront a war that has displaced millions and overwhelmed relief efforts. International...

Will Trump End or Escalate Biden’s Wars?

US President-elect Donald Trump has promised to end wars overseas. But his hawkish cabinet choices will be split over peace...

FO° Exclusive: US Congress Gives Ukraine Sizable, if Not Timely, Aid

Washington’s recent $95 billion aid package to Kyiv will avoid Ukraine’s collapse and NATO’s obsolescence. For now, conflict will continue...

Comment