Recent analysis by the Council on Foreign Relations (CFR) highlights an important shift in the global financial architecture. In their article, “How Cross-Border Chinese RMB Flows May Weaken US Sanctions,” CFR economists Benn Steil and Yuma Schuster argue that the apparent decline in renminbi (RMB) payments recorded by SWIFT does not necessarily signal a weakening international role for China’s currency. Rather, it may reflect the growing use of China’s Cross-Border Interbank Payment System (CIPS) for RMB-denominated cross-border transactions. As more banks participate directly in CIPS and transmit payment messages through its internal network, a larger share of RMB transactions becomes less visible in the Society for Worldwide Interbank Financial Telecommunication (SWIFT) statistics.

According to their analysis, this development carries important geopolitical implications because the US has long relied on the threat of excluding banks from the SWIFT network as a key instrument of financial sanctions. If a growing share of global payments migrates to alternative infrastructures such as CIPS, the effectiveness of this sanctions tool could gradually weaken.

This observation aligns with broader evidence presented by economists at the International Monetary Fund (IMF). Recent IMF staff assessments of China’s economy identify several indicators suggesting that RMB internationalization is progressing gradually. These include rising shares of trade invoicing settled in RMB, increased offshore RMB lending and expanding issuance of “panda bonds” — RMB-denominated bonds issued in China by foreign institutions. Central banks have also modestly increased their holdings of RMB assets as part of broader reserve diversification strategies. Although the RMB still accounts for only a small portion of global financial transactions and foreign-exchange reserves compared with the US dollar, these developments suggest that international currency usage may be slowly diversifying at the margin.

Payment Infrastructure and the visibility of RMB transactions

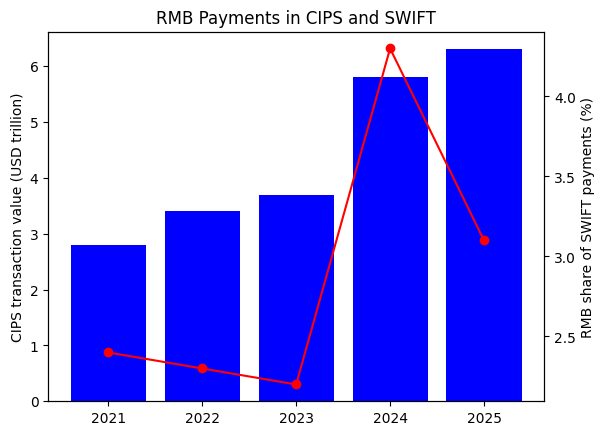

Launched in 2015 by the People’s Bank of China, CIPS functions as a clearing and settlement system for cross-border RMB payments. It also provides messaging services that allow participating banks to transmit payment instructions across borders. In its early years, CIPS remained closely linked to the existing global payment infrastructure. Most CIPS transactions still relied on SWIFT messaging protocols to transmit payment instructions. As recently as 2022, estimates suggested that roughly 80% of CIPS payments were accompanied by SWIFT messages.

Since 2024, however, the structure of the system has begun to evolve. The number of direct participants in CIPS — banks capable of sending payment messages directly through the system — has expanded significantly. Direct participants increased from 139 banks to nearly 193 institutions, representing a growth of roughly 40%. This expansion has gradually shifted the flow of payment messages away from SWIFT and toward CIPS’s internal messaging channels. As a result, a growing share of RMB transactions no longer appears in SWIFT statistics.

This shift helps explain why SWIFT data may underestimate the actual level of cross-border RMB activity. As more payments are processed through CIPS rather than SWIFT, the apparent decline in RMB usage within SWIFT statistics does not necessarily indicate a decline in global RMB transactions. Instead, it reflects a migration of financial messaging infrastructure.

The implications of this migration extend beyond technical changes in payment systems. For decades, the US has exercised significant influence over the international financial system through its central role in global payment infrastructure. SWIFT, though headquartered in Belgium, operates within a financial ecosystem closely tied to Western regulatory frameworks. As a result, access to SWIFT has become an important instrument of economic statecraft. Financial sanctions imposed on countries such as Iran and Russia illustrate the power of this mechanism. By threatening to exclude banks from SWIFT, the US and its allies have been able to restrict targeted countries’ access to global financial markets. In practice, this ability to control access to payment networks has reinforced the international influence of the US dollar.

At the same time, the emergence of alternative payment infrastructures such as CIPS may reduce the effectiveness of this specific strategy at the margin. If more international transactions can be processed through networks outside SWIFT, countries subject to sanctions may find limited ways to maintain financial connectivity despite restrictions imposed through Western-controlled channels. Even so, it would be misleading to interpret such developments as evidence of an imminent decline in dollar dominance. The dollar’s central role in global finance remains supported by much deeper structural factors than payment messaging alone.

US Treasury securities remain the most liquid and widely trusted safe assets in global financial markets. The size and depth of US financial markets continue to provide unparalleled infrastructure for global capital flows, liquidity management and collateral formation. Dollar-based markets also remain central to hedging, derivatives pricing, reserve accumulation and external financing. For these reasons, shifts in payment channels do not automatically translate into a generalized weakening of the dollar’s broader international role.

Structural foundations of dollar dominance

Research from ANZ Research reinforces this perspective. Analysts there argue that even developments such as the potential emergence of a “petroyuan” — oil transactions denominated in RMB — are unlikely to trigger a rapid shift in the global monetary system. If major oil exporters such as Saudi Arabia were to accept RMB as payment for oil exports to China, this could increase the currency’s role in trade settlement and encourage central banks to hold more RMB-denominated assets. However, such changes would more likely represent incremental diversification than a wholesale transformation of the international currency hierarchy.

In this context, this article by your author should not be read as denying the strength or persistence of the dollar. Nor does it attempt to analyze the political dynamics through which the US sustains the dollar as a uniform form of monetary hegemony. Questions concerning the political strategies, institutional coalitions and geopolitical forces that underpin the durability of US monetary power fall outside the scope of the author’s model. Instead, the article adopts a different analytical perspective: It interprets dollar dominance as a form of infrastructure power distributed unevenly across distinct monetary functions within the international monetary system.

From this perspective, the resilience of the dollar derives less from a single hegemonic mechanism than from the dense network of financial markets, legal institutions, safe assets, payment systems and hedging instruments that collectively support global dollar use. The author’s model, therefore, does not deny dollar dominance; rather, it specifies how that dominance operates unevenly across functions. It argues that changes such as the expansion of alternative payment infrastructures, bilateral settlement arrangements or the increased use of non-dollar currencies in trade may permit partial bypass of the dollar in specific domains — especially payments and invoicing — without displacing its central role in more demanding functions such as safe-asset provision, financial anchoring and global liquidity supply.

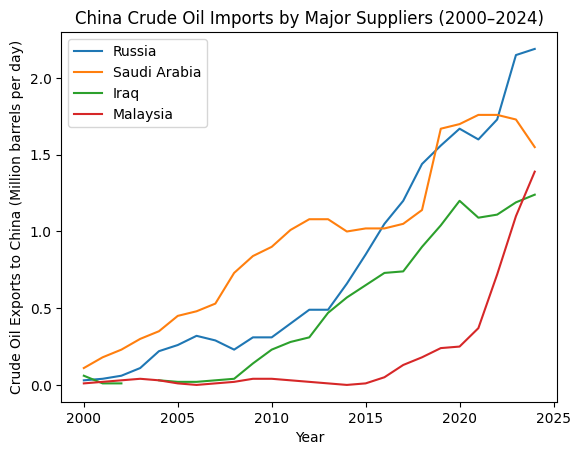

Evidence of such functional reconfiguration can also be observed in the structure of global energy trade. In 2024, Russia, Saudi Arabia, Malaysia and Iraq together accounted for 57.5% of China’s crude oil imports. Russia emerged as the largest supplier, exporting approximately 2.19 million barrels per day (Mb/d) of crude oil to China — about 41% more than Saudi Arabia’s 1.55 Mb/d. Malaysia and Iraq followed with exports of 1.39 Mb/d and 1.24 Mb/d, respectively. Together, these four countries supplied more than half of China’s crude oil imports. Notably, Malaysia overtook Iraq by roughly 12% in exports to China despite not being a major oil producer. This pattern has led analysts to suggest that part of these exports may include Iranian crude oil rebranded as Malaysian in order to circumvent international sanctions.

Such trade patterns are closely linked to sanctions evasion and the diversification of transaction routes. Countries subject to Western financial sanctions — most notably Russia and Iran — have increasingly sought to reduce their dependence on dollar-denominated settlement and Western financial infrastructure by utilizing alternative payment channels, including renminbi-based settlement arrangements and non-Western payment networks. As a result, a portion of energy transactions has begun to shift toward settlement in RMB or other non-dollar currencies.

However, these developments remain concentrated primarily in the transactional functions of international money — specifically the medium-of-exchange and unit-of-account roles associated with trade settlement and pricing. Even in global oil markets, more demanding financial functions such as hedging, liquidity provision, asset management and safe-asset holdings remain overwhelmingly anchored in the dollar-based financial system. The deep liquidity of US financial markets, the availability of dollar-denominated safe assets, and the extensive infrastructure for derivatives and risk management continue to reinforce the dollar’s central role.

Consequently, the expansion of RMB settlement in China’s energy trade should not be interpreted as evidence of the collapse of the dollar-based international monetary system. Rather, it reflects a limited redistribution of payment infrastructure and currency usage within specific transactional domains. The dollar continues to occupy the core of global financial architecture, even as alternative currencies and payment systems gradually expand their presence in selected areas of trade and settlement. The emerging international monetary system, therefore, appears increasingly layered, characterized by partial diversification in transactional functions while the deeper financial foundations of dollar dominance remain firmly intact.

Historical experience also suggests that major shifts in global currency regimes occur only under extraordinary institutional and geopolitical circumstances. The rise of the US dollar as the dominant international currency was closely tied to the creation of the Bretton Woods system in 1944 and the broader economic and political order that emerged after World War II. Similarly, the decline of the British pound as the leading reserve currency accelerated only after major geopolitical shocks such as the Suez Crisis in 1956.

In contrast, the contemporary international financial system lacks a comparable institutional turning point that would facilitate the rapid replacement of the dollar. Moreover, China itself appears cautious about fully internationalizing the RMB. Rather than pursuing rapid financial liberalization, Chinese policymakers have generally favored a gradual approach centered on trade settlement, regional financial links and selective infrastructure development. The expansion of CIPS, along with initiatives such as the digital renminbi (e-RMB), reflects efforts to build alternative transactional channels without fully opening China’s capital account.

For this reason, the evolution of financial infrastructure may prove more significant than the immediate expansion of RMB-denominated transactions. Although CIPS currently processes only a small fraction of the daily transaction volume handled by SWIFT, its growth signals a broader trend toward diversification in global payment networks. Geopolitical fragmentation may reinforce this process, as countries increasingly seek to reduce vulnerability to sanctions and network exclusion.

Ultimately, the expansion of CIPS and the gradual growth of RMB usage point to a broader transformation in the architecture of global finance. Yet this transformation is better understood as functional diversification within a still dollar-centered system than as a generalized transition away from dollar dominance. The central question for policymakers, therefore, is not whether the RMB will soon replace the dollar. It is how the diversification of global financial infrastructure may reshape the distribution of power within an international monetary system whose deepest financial foundations remain anchored in the dollar.

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

The Dollar at a Crossroads: Trade Wars, Tariffs and Stress on the World’s Safe-Haven Currency

The US dollar’s dominance has rested on America’s economy, strong institutions and deep financial markets, which made dollar assets the...

Hong Kong Dollar Peg to Chinese Yuan: A Pragmatic Shift or Risky Gamble?

Hong Kong’s 42-year-old dollar peg holds firm, but the ground beneath it is shifting. As the city deepens ties with...

The Long-Term Dangers of China’s Expanding Swap Line Strategy: Financial Dependence and Geopolitical Influence

China’s currency swap strategy expands its financial influence by creating economic dependencies. While these agreements provide liquidity to struggling economies,...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment