Mutual funds let you pool your money with other investors to “mutually” buy stocks, bonds and other investments. They’re run by professional money managers who decide what to buy — stocks and bonds in various markets — and what to sell. They also decide when to buy and sell assets on behalf of their investors.

Mutual funds began in the US a century ago. This financial instrument in 1924 was popular with our parents’ generation. Their advantages include diversification, professional management, affordability, daily liquidity, variety of choices by region, sector, company size or investment style and automatic reinvestment of dividends and capital gains.

However, most mutual funds come with considerable up-front sales charges as well as annual fees, eating into returns over longer periods. Making matters worse, up to 96% of all active US equity funds underperformed their benchmark over a 15-year period, as described in this earlier article. They underperform the market.

The emergence of ETFs

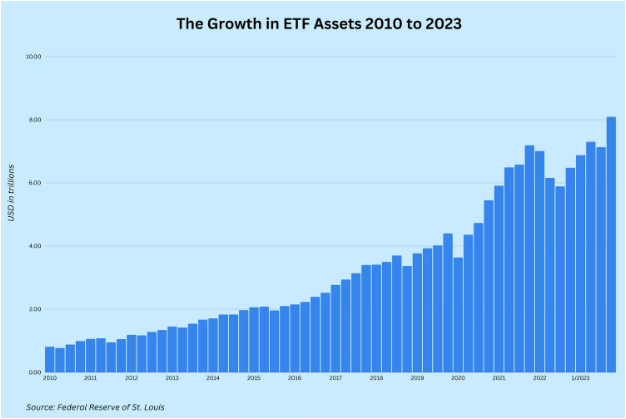

A relatively new type of fund has been cannibalizing mutual funds in recent years. Known as exchange-traded funds (ETFs), the first such fund was launched in Canada in 1990. In 1993, the first ETF was launched in the US. ETFs took time to catch on before growing rapidly in popularity. They seek to track an index, which is typically weighted as per market capitalization, in order to capture the risk and return of a given market. ETFs comprised only 1% of total fund trading in 2000. The crash of the dotcom bubble in 2001 boosted the popularity of ETFs, and a graph on the popular site Investopedia reveals that they have really taken off since 2010.

Since most mutual funds underperform the market and ETFs are largely so-called passive investment vehicles that replicate the market, why would someone pay higher fees for an inferior performance?

Before we carry on, it is important to understand what active and passive investment means. “Active” describes the process of actively selecting a few stocks, hoping their performance would beat a broad index, like the S&P 500. “Passive”, on the contrary, involves simply replicating the performance of said index. Once funds are invested according to the weights prescribed by the index, the manager can fold his hands and remain passive.

Why do ETFs perform better and what are the risks?

Why are an increasing number of investors switching to so-called passive investment vehicles? Since there is no need to do any security research, passive ETFs can do without hiring expensive analysts. This allows them to charge much smaller fees and outperform the mutual funds.

The State Street Global Advisors SPDR S&P 500 ETF Trust (symbol “SPY”), with more than $500 billion in assets, charges annual fees of less than a tenth of one per cent, ie <0.1%. By contrast, Capital Group’s “Growth Fund of America,” the largest active US equity mutual fund, carries an expense ratio of 0.63% — more than 6 times as much as “SPY.” In addition, investors in the active fund need to digest a front-load of up to 5.75%.

Unsurprisingly, passive ETF have been cannibalizing active mutual funds over the past years. Conversely, since 2017, US equity mutual funds had only one month of net inflows, and 87 months of outflows.

According to fund analytics firm Morningstar, active US equity funds saw outflows of $290 billion over the past 12 months, while their passive counterparts enjoyed inflows of $320 billion. Passively managed equity vehicles now make up more than 60% of the total funds invested in markets.

As the share of passively managed investment grows, so does their ownership of individual stocks. In some companies, passive investors are already in the majority. Take Central Garden and Pet (symbol “CENT”), for example, where 60% of shares are owned by passive vehicles. Those funds are not interested in the fundamentals of the company such as sales, earnings or dividends. The company might announce terrible results, and passive investors would not sell a single share. It could, theoretically, be approaching bankruptcy, and, as long as the company remains in the index the fund tracks, the fund would not sell.

Passive investment vehicles are insensitive to price. They are always fully invested. If fresh money comes in, the funds buy no matter what. Regular contributions to retirement accounts (“401k”) lead to a continuous stream of money driving index members share prices regardless of fundamentals.

As more investors become price insensitive, you expect to see more “crazy” price movements, leaving rational investors scratching their head. A rally induced by the recent index inclusion of Super Micro Computer (symbol SMCI) serves as an example. The company’s stock price rose from $284 at the end of 2023 to $1,229 on March 8, 2024, shortly before its inclusion into the S&P 500 Index on March 18. It has since lost around 37% of its value.

Erratic price movements could lead to the impression fundamentals did not matter anymore. Inexperienced investors might be tempted to bet on so-called “momentum” stocks, or worse, options, with quickly eroding time value.

Of course, indiscriminate inflows could reverse. An aging population of investors might want to cash out of stocks, realizing their capital gains. Persistent outflows would lead to selling, with the sellers, again, being insensitive to price.

So, are ETFs a cure, or rather a curse in disguise?

Low-fee, passive index ETF are the most efficient investment vehicle available to individual investors. For each individual the decision to move into passive ETF is, undoubtedly, rational. However, individual rational behavior doesn’t guarantee a rational outcome in aggregate. For investors as a group, the outcome might be detrimental.

[Fair Observer’s interns, working as a team, edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

How Volatility Makes Closely Held Firms Misallocate Money

Closely held companies more reactive to volatility in their stock price than other firms. When they anticipate volatility, they tend...

Why Foreigners Want US Securities — But Not Dollar Exposure

Foreign investors are allocating ever-higher shares of their portfolios to US dollar-denominated securities, but not necessarily because they want to...

How to Invest: Forget the Needle, Buy the Haystack

Individual and professional investors alike have been underperforming benchmark indices for decades. Explanations brought forward include Efficient Market Hypothesis, behavioral...

Impact Investment Is a Promising Way Forward for India

Impact investing can significantly improve the lives of people in the developing world while making respectable returns for investors. Nowhere...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Why Capitalism Failed in the Ottoman Empire and the Turkish Republic

Turkey’s economic struggles arise from a bureaucratic tradition that favors state control over the creative destruction essential for capitalism. Political...

The Enduring Relevance of Development Economics in an Unequal World

Some economists argue that as developing countries’ incomes rise and mainstream economics converge with development studies, the distinctiveness of development...

Sustainable Next-Gen Material Tech Makes for a Better Consumer Market

The nascent next-generation materials industry, helmed by nearly 150 companies worldwide, is set to dethrone unsustainable animal-based materials. Industry investment...

Comment