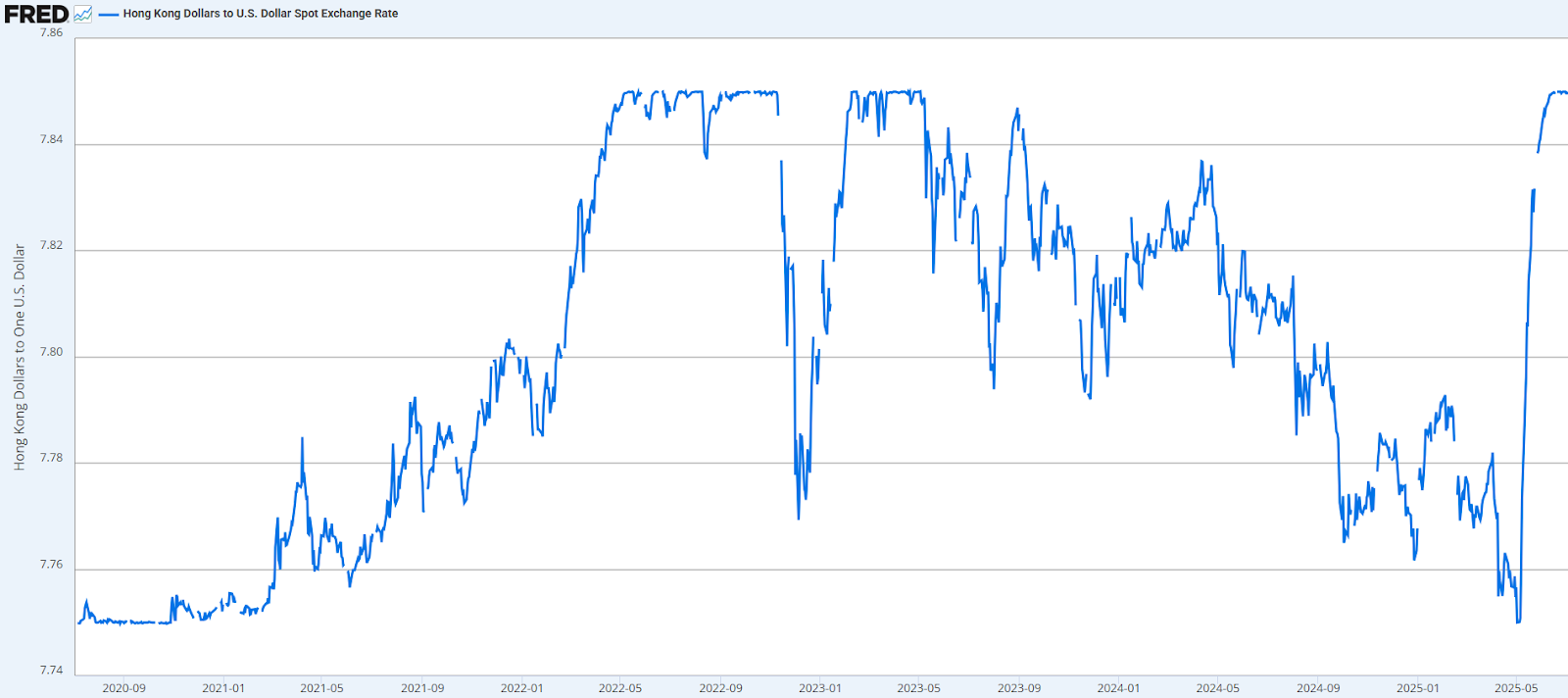

Since 1983, the Hong Kong dollar (HKD) has been anchored to the US dollar (USD) via the Linked Exchange Rate System (LERS). This is a robust currency board arrangement underpinned by full reserve backing — US dollar reserves fully back the amount of Hong Kong dollars issued. Operated under a strict, transparent and resilient Currency Board framework, the system maintains the stability of the Hong Kong dollar within a narrow band of $7.75 to $7.85 HKD per USD, because of the arrangement’s automatic convertibility. This regime has provided Hong Kong with remarkable monetary stability, even through the Asian Financial Crisis, SARS outbreak and the Global Financial Crisis. The LERS, institutionalized through the Hong Kong Monetary Authority (HKMA), embodies a monetary commitment mechanism that substitutes for a domestic monetary policy by importing US credibility.

However, economists are now scrutinizing this longstanding system. Over the past decade, Hong Kong has accelerated its economic integration with mainland China. The Greater Bay Area initiative has deepened cross-border financial links, while the Chinese yuan (CNY) — especially the offshore Hong Kong variant — has gained ground in global settlements. Simultaneously, US–China tensions have elevated systemic risks in dollar-reliant jurisdictions. These dynamics prompt a fundamental question: Should Hong Kong realign its currency anchor from the USD to the CNY?

That question is no longer purely academic. In early May 2025, the HKMA injected over $60.5 billion HKD into the market to defend the peg — the nation’s currency tied to the exchange rate of another nation — as the HKD again approached the weak-side limit of 7.85. Over the course of a single week, Bloomberg estimates that the HKMA injected approximately $59 billion HKD (around $7.5 billion) through three separate FX interventions to stabilize the Hong Kong dollar.

This piece assesses the merits and hazards of shifting to a yuan peg through the lenses of macroeconomic theory, financial market modeling and political economy.

What derivatives markets reveal about peg fragility

One of the clearest ways to gauge investor sentiment about Hong Kong’s currency regime is by looking at how financial markets are pricing risk — especially through derivatives such as currency forwards and options. These instruments give us real-time insight into whether investors believe the HKD peg to the USD will hold, or whether they expect it to break.

When investors believe that a pegged currency might soon move to a floating regime or shift to a new anchor — like the CNY — this uncertainty shows up in option prices. Specifically, options that protect against large swings in the HKD become more expensive. By analyzing these prices, economists and central banks can estimate what probability the market is assigning to a potential regime change.

Recent data suggest that this probability is rising. As of mid-2025, markets are increasingly pricing in the possibility that the HKD–USD peg may not be sustainable indefinitely. One metric used by FX desks is the risk reversal — the difference in price between buying an option to hedge a stronger HKD and one to hedge a weaker HKD. This measure has become more skewed to the downside, signaling growing concern about depreciation risks or a future realignment of the peg.

Another red flag is the cost of non-deliverable forwards (NDFs) — contracts used to speculate on or hedge future exchange rates where capital controls or uncertainty exist. NDF pricing on the HKD is showing wider spreads compared to past norms, suggesting markets are hedging against more volatility than usual. These changes closely track rising global interest rate differentials, declining liquidity in Hong Kong’s banking system and heightened political uncertainty.

In short, while the peg remains intact, market-based indicators are flashing caution. They reflect growing skepticism about how long the HKMA can defend the current system without introducing new policy tools or considering structural adjustments.

To help interpret these signals, economists sometimes use simplified models that estimate what investors think might happen under different scenarios, such as the peg continuing versus a re-pegging to the yuan. Based on this approach, one estimate suggests that markets now see a nearly 50% chance of peg discontinuity in the medium term — levels last seen during the 2008 Global Financial Crisis.

Moreover, if the peg were abandoned, market pricing suggests that the HKD would likely move closer in value to the yuan rather than float freely. This is a striking development: It signals that in the event of a change; investors are already anticipating closer monetary alignment with China.

This doesn’t mean a shift is inevitable. But it does highlight the value of these market-based signals in providing early warnings to central bankers and FX officials. Peg regimes are as much about credibility and perception as they are about reserves and policy rules. If markets start to doubt the HKMA’s ability or willingness to maintain the peg, it can create a self-fulfilling pressure, even if the fundamentals remain strong.

The takeaway is clear: The HKD–USD peg is still holding, but the risk premium for holding HKD is rising. This should prompt careful monitoring and timely communication by the HKMA to reinforce market confidence.

Strategic realignment or premature gamble?

Proponents of a yuan peg cite three major rationales:

- Economic integration: Over 50% of Hong Kong’s trade in 2024 was conducted with mainland China. Financial linkages through Stock Connect, Bond Connect and Wealth Management Connect have cemented bilateral capital flows. Pegging to the yuan would reduce transaction costs and FX hedging complexity for firms operating across the border.

- Renminbi internationalization: As China scales up its Cross-Border Interbank Payment System (CIPS) and e-CNY pilots, Hong Kong could serve as a premier offshore settlement hub. A yuan peg would position Hong Kong as an institutional anchor in the global de-dollarization trend, particularly in Belt and Road economies.

- Geopolitical hedging: Amid intensifying US–China strategic rivalry, Hong Kong faces increasing risks of secondary sanctions, export restrictions and financial surveillance. A yuan peg might shield its financial system from such external shocks by reducing direct reliance on dollar-based clearing and custody systems.

However, the counterarguments are formidable:

- Capital account constraints: The yuan remains only partially convertible. Although China has liberalized under the Qualified Foreign Institutional Investor (QFII) and RMB Qualified Domestic Institutional Investor (RQDII) schemes, the People’s Bank of China (PBOC) retains discretionary capital controls. Pegging to a non-convertible currency undermines the viability of any credible board-like regime.

- Policy opacity: The PBOC’s exchange rate regime is a managed float with daily midpoint settings and periodic direct intervention. This contrasts sharply with the HKMA’s rule-bound and transparent operations. Importing such opacity would erode investor confidence in Hong Kong’s financial governance.

- Legal and institutional risks: The HKD–USD peg is embedded in legal contracts, the International Swaps and Derivatives Association (ISDA) documentation — the global standard for derivatives contracts — and derivative clearing systems. Transitioning the anchor currency would require massive contractual rewrites and could trigger systemic counterparty risk.

- Geopolitical blowback: A yuan peg would likely be interpreted as a de facto political realignment with Beijing. This could provoke US sanctions or trigger the removal of Hong Kong’s special trading status under US and EU law, with substantial ramifications for multinational financial institutions.

Navigating the trilemma with gradualist alternatives

The Hong Kong case vividly illustrates the “impossible trinity” or monetary trilemma: A jurisdiction cannot simultaneously maintain free capital mobility, a fixed exchange rate and monetary policy autonomy. By design, Hong Kong sacrifices monetary independence in favor of a credible peg and open capital account.

Switching to a yuan peg would not resolve this trilemma, but merely substitute one constraint for another. It would replace imported Federal Reserve policy with alignment to PBOC settings, which lack transparency and could respond to non-market criteria. Furthermore, given China’s reactive capital control framework, Hong Kong would likely face episodic arbitrage pressures from exchange rate misalignments, settlement delays or inefficiencies in cross-border transactions, and liquidity challenges due to capital flow restrictions.

Instead of abrupt realignment, a suite of gradualist alternatives offers a path forward:

- Dual anchor framework: Hong Kong could maintain its dollar peg while simultaneously promoting CNY usage in trade finance and settlement. By gradually building a parallel renminbi ecosystem, Hong Kong could prepare for deeper future integration without destabilizing the existing regime.

- Currency basket peg: Pegging the HKD to a weighted basket (e.g., 60% USD, 30% CNY, 10% EUR) would enhance resilience and reflect actual trade patterns. However, such a system would reduce transparency, complicate intervention mechanics and risk speculative attack during transitions.

- Monetary buffering and market signaling: Enhancing FX reserves, publishing real-time intervention data and tightening the peg band during crisis periods could restore market confidence in the existing system. The implied volatilities and skew — the latter being the difference in implied volatility between a currency pair’s call and put options — of FX option market monitoring can provide the HKMA with forward-looking risk indicators. If the implied volatility on USD calls (due to a weakening HKD) rises sharply compared to puts, it signals market fears of a potential peg break or devaluation.

- Digital currency integration: Participation in digital yuan pilots without formally shifting the peg could allow Hong Kong to shape regional fintech architecture while preserving its dollar-based monetary firewall.

Stability, optionality and trust

Currency regimes do not operate in a vacuum. They rest on institutional credibility, strategic foresight and geopolitical alignment. While markets increasingly price the potential for a peg shift, the underlying architecture of the LERS remains sound. Hong Kong holds over $430 billion in reserves — more than twice its monetary base — and its legal and policy frameworks continue to command global investor trust.

The deeper question is whether Hong Kong can continue to serve as a bridge between two incompatible monetary systems — liberal, rule-based dollar finance and state-centric, capital-managed yuan finance — without compromising either. For now, the answer lies in preserving optionality.

The HKD–USD peg has delivered nearly 42 years of macroeconomic stability, low inflation and international integration. The political costs of abandoning this legacy — especially in the absence of full yuan convertibility — far outweigh the speculative benefits. Indeed, a premature shift could backfire, accelerating capital flight, destabilizing asset prices and reducing Hong Kong’s appeal as a financial platform.

Instead, the pragmatic path is strategic patience. Rather than adopting the yuan as anchor, Hong Kong should deepen its role as a multipolar financial node — supporting dollar, yuan and digital rails alike. Over time, if and when the yuan becomes fully convertible, independently priced and broadly accepted as a global reserve asset, the peg debate can be revisited with a more balanced risk-reward profile.

Until then, the US dollar remains the bedrock not just of Hong Kong’s exchange rate, but of its institutional trust and global stature.

The future of the peg

The debate over whether to reanchor the Hong Kong dollar from the US dollar to the yuan is not merely a technical question of exchange rate policy — it is a reflection of deeper global tensions. At stake is more than monetary alignment; it is a test of how to operate between two diverging systems: one grounded in liberal, rules-based transparency, and the other shaped by state-driven capital controls and strategic ambiguity.

Hong Kong stands uniquely at the crossroads of this global transition. It is not just a currency regime under scrutiny, but an institutional model under stress, caught between competing geopolitical narratives and market logics. The HKD–USD peg, in place since 1983, has served not only as a nominal anchor, but as the backbone of Hong Kong’s credibility as an international financial center. As integration with the mainland deepens and global monetary structures fragment, that foundation is increasingly under market-led reassessment.

This is not a moment for premature decisions or symbolic realignment. The core challenge is not choosing between the dollar or the yuan, but maintaining institutional coherence in a world where the political, financial and reputational costs of miscalculation are rising. Strategic patience, not reactive allegiance, must define the path forward.

In a time of fluidity and fractured certainties, stability no longer means inaction — but neither does movement without clarity ensure progress. For now, the peg endures. What ultimately sustains it may not be just reserves or rules, but trust — earned, maintained and constantly tested.

[Lee Thompson-Kolar edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

The History and Political Context of the Japan–South Korea Currency Swap Line

The Japan–South Korea currency swap line has been a key instrument for financial stability and economic cooperation since 2001. However,...

The Long-Term Dangers of China’s Expanding Swap Line Strategy: Financial Dependence and Geopolitical Influence

China’s currency swap strategy expands its financial influence by creating economic dependencies. While these agreements provide liquidity to struggling economies,...

Reshoring: Reality or Myth? US–China Trade and the Future of American Manufacturing

US manufacturing is at a crossroads, shaped by tensions with China and technological shifts like AI and automation that are...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment