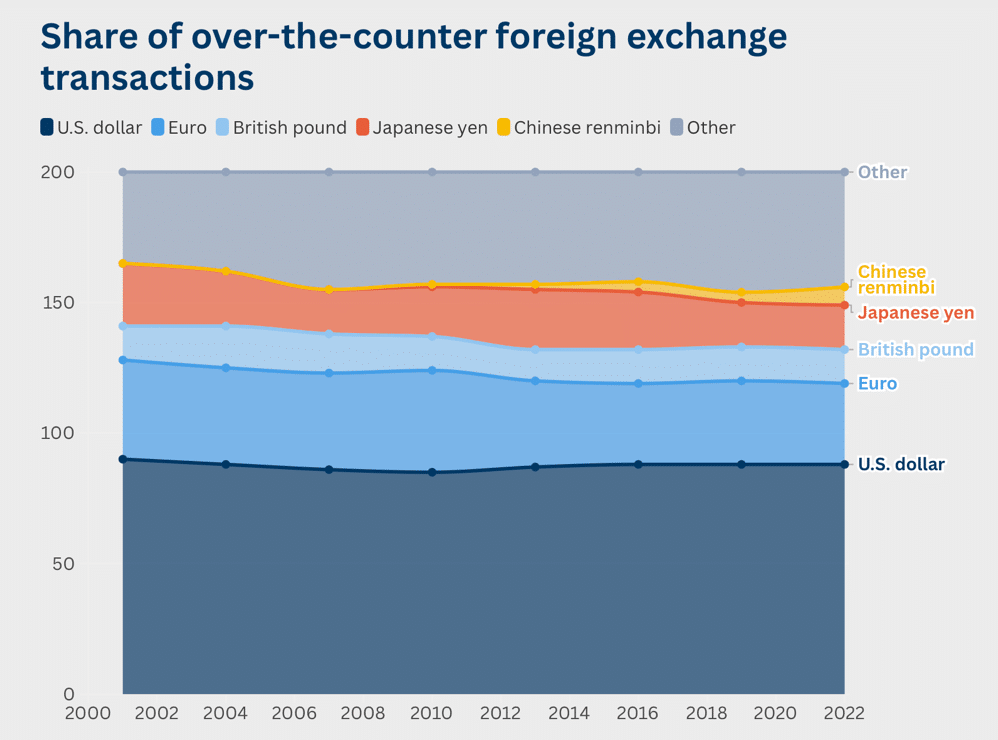

The US dollar is often described as the world’s reserve currency, but that description understates its true role. It is not simply a unit of account or a medium of exchange — it is the underlying infrastructure of the global economy. A more accurate metaphor is a river: vast, dynamic and shaping the terrain through which it flows. Nations do not merely use the dollar; they operate within its currents. Trade is invoiced in it, reserves are held in it and financial systems depend on its liquidity. According to the Bank for International Settlements (BIS), the dollar is involved in nearly 88–90% of all foreign exchange transactions, far exceeding the economic weight of the US itself. This overrepresentation is not incidental — it is the foundation of American monetary power.

Yet this power is paradoxical. The US issues the world’s dominant currency, but it does not fully control its consequences. Global demand for dollar liquidity, safety and credibility determines its strength as much as domestic policy does. As a result, policymakers are left attempting to steer a system that reacts to forces beyond their reach. Like a river, the dollar can be guided, influenced and redirected at the margins — but it cannot be held still or commanded outright. This structural reality defines both the strengths and limitations of American economic leadership.

Domestic economic and political tensions

At the domestic level, the dollar’s strength produces a subtle but persistent transformation of the US economy. A strong dollar lowers the cost of imports, suppresses inflation and attracts global capital into US financial markets. This creates a sense of stability and prosperity: consumers benefit from cheaper goods, asset prices rise and inflation remains contained. But beneath this surface, the structure of the economy begins to shift. As the dollar appreciates, US exports become more expensive in foreign markets, reducing external demand for domestically produced goods. Manufacturing sectors face sustained pressure, not through sudden collapse but through gradual erosion. Production yields ground to consumption, and the economy becomes increasingly oriented toward finance rather than industry.

This dynamic is not merely economic; it is political. The dollar redistributes benefits and costs across different groups. Financial institutions, asset holders and consumers gain from a strong currency, while export-oriented industries and manufacturing workers face structural disadvantages. The result is a persistent tension within the domestic economy, one that cannot be resolved through simple policy adjustments. A weaker dollar might support industrial competitiveness and export growth, but it would also raise import prices and risk inflation. A stronger dollar stabilizes prices but deepens the shift toward financialization. There is no optimal equilibrium — only a continuous balancing of competing objectives.

This tension is reinforced by the constraints it places on monetary policy. The Federal Reserve does not directly set the value of the dollar, but its decisions shape global capital flows. Higher interest rates attract foreign investment, strengthening the dollar and tightening financial conditions worldwide. Lower rates may ease upward pressure, but they can also trigger capital outflows and weaken confidence. The relationship is circular: The dollar influences inflation, and inflation constrains monetary policy. For example, a weaker dollar raises import prices, contributing to inflationary pressure, which in turn forces the central bank to maintain tighter policy. The currency thus operates as a feedback loop rather than a controllable instrument.

Global power and strategic responses

The complexity deepens when the dollar is viewed in its global context. It functions as the backbone of an extensive financial network, linking banks, corporations and governments across borders. Institutions such as the Society for Worldwide Interbank Financial Telecommunications (SWIFT) facilitate this system, enabling transactions that are overwhelmingly denominated in dollars. The result is a form of infrastructural power that is both pervasive and largely invisible. The US does not need to intervene directly in every transaction; its influence is embedded in the system itself.

This embedded power becomes most visible in the use of financial sanctions. By restricting access to dollar-based systems, the US can exert pressure on other countries without deploying military force. This strategy has been used across administrations, from former President Barack Obama to current President Donald Trump, reflecting its effectiveness as a tool of statecraft. When access to the dollar is limited, the impact extends beyond the immediate target. Financial institutions, multinational corporations and even neutral countries adjust their behavior to avoid exposure, amplifying the reach of US policy. In this sense, the dollar operates as a global gatekeeper.

However, this power is not without cost. The more the dollar is used as an instrument of coercion, the more it reveals the risks associated with dependence on it. Other countries, observing the reach of US financial sanctions, have begun to seek ways to reduce their exposure. This does not mean abandoning the dollar altogether — its advantages remain unmatched — but it does mean building alternatives that can function in parallel. These alternatives are not replacements; they are safeguards.

Nowhere is this dynamic more evident than in China’s strategy under President Xi Jinping. China has pursued the development of financial systems that can operate independently of dollar-based infrastructure. The Cross-Border Interbank Payment System (CIPS) allows for renminbi-denominated transactions outside traditional Western channels, while digital currency initiatives aim to create new mechanisms for cross-border settlement. As Xi has emphasized, “a powerful currency that can be widely used in international trade, investment and foreign exchange markets, and attain reserve currency status.” This approach is not about immediate dominance but about long-term resilience. It recognizes that in a system where financial infrastructure can be weaponized, dependence itself becomes a strategic risk.

A similar logic is emerging in Europe, though with a different emphasis. President of the European Central Bank Christine Lagarde has framed the development of a digital euro as more than a technological innovation. “It is a political statement concerning the sovereignty of Europe,” she has argued, highlighting the connection between monetary systems and strategic autonomy. The euro already accounts for roughly 20% of global foreign exchange reserves, according to the International Monetary Fund (IMF), making it the second most important currency after the dollar. But its role remains constrained by fragmented financial markets and institutional limitations within the EU. Efforts to deepen integration and modernize payment systems are therefore not just economic initiatives — they are attempts to reduce reliance on external infrastructure and enhance Europe’s position in a changing global order.

Lagarde has cast the digital euro as a sovereignty project, a logic that also informs attempts to integrate the EU’s capital markets. As these efforts move forward, the euro could attract wider international use, especially from those seeking alternatives to a dollar system perceived as increasingly politicized.

Recent events suggest that the global economic landscape is entering a more defensive phase. US Vice President JD Vance convened ministers from more than 50 countries at the first Critical Minerals Ministerial, signaling Washington’s urgency in countering China’s dominance over rare-earth supply chains. Beijing, for its part, has been advancing a parallel strategy. Days earlier, Qiushi, the Chinese Communist Party’s flagship journal, published a speech by Xi calling for the renminbi to “attain reserve currency status,” while regulators quietly encouraged banks to scale back purchases of US Treasury bonds.

These moves, though different in form, point in the same direction: a growing effort by major powers to reduce strategic dependence and secure greater control over critical economic levers. As Canadian Prime Minister Mark Carney has suggested, such dynamics can leave smaller states with little choice but to align defensively. Yet even this interpretation does not fully capture the moment. The deeper shift is that vulnerability is no longer asymmetric. In a system where finance, currencies and supply chains can be weaponized, even the largest economies are increasingly aware of their own exposure.

It is this shared sense of fragility — not just competition — that is beginning to reshape policy. Governments are no longer acting solely to expand influence, but to limit risk, hedge against disruption and insulate themselves from external pressure. The result is a global system that feels less stable, more fragmented and increasingly driven by precaution rather than confidence.

These developments reflect a broader transformation in the nature of globalization. In the past, economic integration was pursued primarily for efficiency and growth. Supply chains were optimized, financial systems interconnected and dependencies deepened. Today, those same dependencies are increasingly viewed as vulnerabilities. Countries are no longer concerned only with maximizing gains from trade and finance; they are also focused on minimizing exposure to external control. The global system is shifting from one defined by interdependence to one shaped by strategic competition.

Erosion, confidence and the future of the dollar

This shift creates a feedback loop that complicates the exercise of American power. Each time the US uses the dollar as a tool of coercion, it strengthens the incentive for others to develop alternatives. These alternatives, in turn, reduce the effectiveness of future actions. The process is gradual but cumulative. It does not lead to a sudden collapse of dollar dominance, but to a slow erosion of its centrality. The river does not disappear — it begins to branch.

The durability of the dollar ultimately depends on confidence. According to the IMF, the dollar still accounts for approximately 58% of global foreign exchange reserves, far exceeding any competitor. This reflects not only economic fundamentals but institutional credibility. US financial markets are deep and liquid, legal systems are relatively stable and the dollar remains the default currency for global transactions. These factors create a self-reinforcing system: The more the dollar is used, the more valuable it becomes.

But confidence is not immutable. It is shaped by experience, and repeated exposure to the risks of financial coercion may gradually alter perceptions. Countries do not need to abandon the dollar to reduce its influence; they need only diversify enough to create alternatives. Even a partial shift can change the balance of power over time.

In this evolving landscape, the challenge for the US is not to maintain absolute control but to manage a system that is inherently dynamic. The dollar’s strength lies in its centrality, but that centrality depends on trust as much as on power. Overuse of financial leverage risks undermining that trust, while underuse may limit the ability to respond to geopolitical challenges. The task is therefore one of balance — preserving the benefits of dominance without accelerating its erosion.

The metaphor of the river captures this challenge precisely. The dollar flows through the global economy, shaping and being shaped by the forces around it. It carries immense power, but that power is diffuse and contingent. Policymakers can influence its direction, but they cannot fix its course. Attempts to do so risk destabilizing the system itself.

In the end, the dollar is not just a currency; it is a reflection of a broader reality about power in an interconnected world. It is fluid rather than fixed, relational rather than absolute and always subject to change. The US remains at the center of this system, but the nature of that center is evolving. The river still runs through it — but the channels are widening, the currents are shifting and the task of navigation is becoming more complex with each passing year.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

China’s Use of Renminbi and CIPS Challenges US Dollar but Falls Short

Council on Foreign Relations economists argue that SWIFT data showing a decline in renminbi payments is misleading. Renminbi-denominated transactions might...

The Politics of Cheapness: Japan’s Consumption-Tax Truce, the Yen’s Fragility and the Long Shadow of a Weaker Dollar

Japan’s cross-party push to cut the consumption tax ahead of the February 2026 election reflects the seductive politics of cheapness,...

The Dollar at a Crossroads: Trade Wars, Tariffs and Stress on the World’s Safe-Haven Currency

The US dollar’s dominance has rested on America’s economy, strong institutions and deep financial markets, which made dollar assets the...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Gold at $4,000: The Price of Fiscal Dominance

Gold’s surge above $4,000 reflects eroding confidence in fiat currencies as fiscal deficits expand and central banks face political pressures....

Will Takaichi’s Risky Opposition Now Challenge Ishiba’s Economic Reform?

Newly-elected Prime Minister Shigeru Ishiba and Governor Kazuo Ueda support the Bank of Japan, championing cautious economic policy without direct...

Central Bank Independence Is Unbelievably Valuable for the World Economy

To ensure sound monetary policy and economic stability, central banks like the US Federal Reserve need their independence (CBI). Opposing...

Comment