The global economy has entered a period characterized by persistent trade imbalances, elevated geopolitical tensions, fragmented supply chains and growing uncertainty surrounding the future of the international monetary system. Traditional prescriptions for correcting external imbalances — exchange-rate flexibility, structural reforms and fiscal adjustment — have produced only modest results over the past two decades.

Instead, governments have increasingly relied on tariffs, industrial policy, export controls and financial sanctions to address external vulnerabilities. While these instruments may generate short-term political gains, they rarely address the underlying macroeconomic sources of persistent external imbalances.

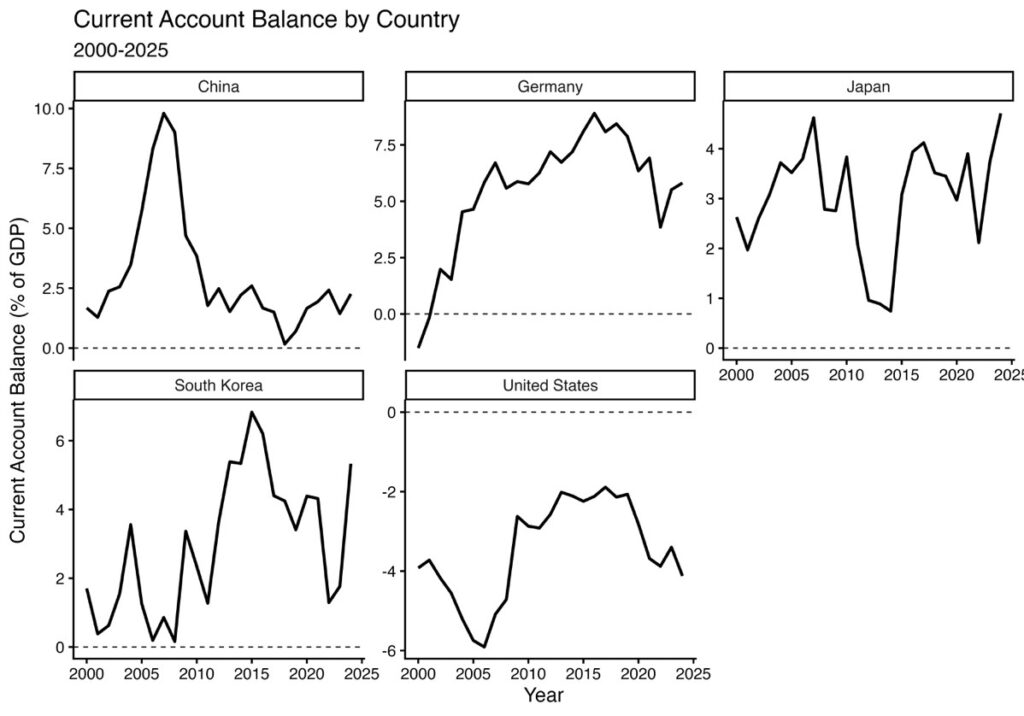

Figure 1 illustrates the persistence of these imbalances among the world’s major economies. As shown, Germany, Japan, South Korea and China have generally maintained current-account surpluses throughout the past two decades, although the magnitude of these surpluses has varied over time. By contrast, the US has consistently recorded sizable current-account deficits.

Despite major global events — including the Global Financial Crisis, the COVID-19 pandemic and geopolitical disruptions — the overall pattern of surplus and deficit economies has remained remarkably stable. The persistence of these external positions suggests that global imbalances reflect deeper structural forces rather than temporary cyclical fluctuations.

Recent discussions surrounding Asian exchange rates have revived an issue that has received insufficient attention since the aftermath of the 1985 Plaza Accord: the strategic role of coordinated currency intervention. The proposition that coordinated appreciation of undervalued Asian currencies can reduce persistent external surpluses has often been dismissed as an outdated policy framework.

Nevertheless, the persistence of the imbalances illustrated in Figure 1 suggests that existing adjustment mechanisms have been insufficient. As global current-account surpluses have become increasingly concentrated among East Asian economies while the US continues to absorb global demand through sustained current-account deficits, exchange-rate coordination deserves renewed consideration as part of a broader strategy for restoring balance to the international monetary system.

The exchange rate–current account nexus

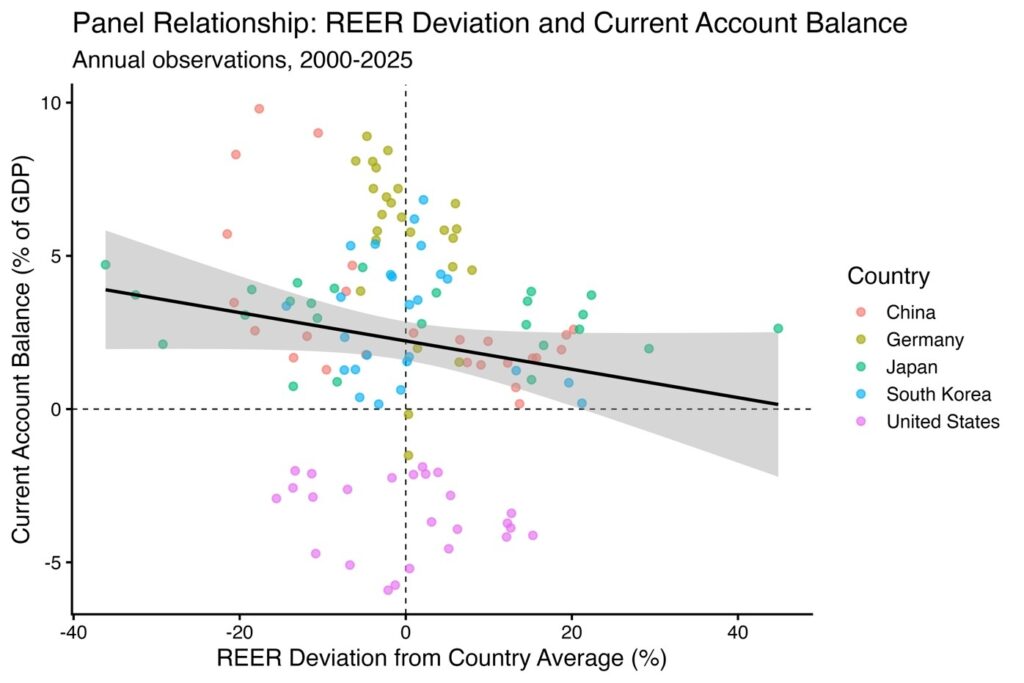

Figure 2 provides an overview of the relationship between movements in the real effective exchange rate (REER) and current account balances across five major economies — the US, China, Japan, Germany and South Korea — using annual observations from 2000 to 2025. Each point represents a country-year observation, while the fitted regression line summarizes the average relationship across the full sample.

A clear negative relationship emerges from the data. Periods when a country’s real effective exchange rate is relatively stronger than its long-run average are generally associated with weaker current account balances. Conversely, periods of relative currency weakness tend to coincide with stronger external positions. Although the observations exhibit considerable variation across countries and over time, the overall downward trend is both visually apparent and economically meaningful.

This pattern is consistent with one of the central propositions of international macroeconomics. Changes in the real exchange rate alter the relative prices of domestic and foreign goods, thereby influencing international competitiveness. A stronger currency tends to reduce export competitiveness while making imports relatively less expensive, placing downward pressure on the trade balance and, ultimately, the current account. By contrast, a weaker currency generally enhances export competitiveness, encourages import substitution and contributes to stronger external balances.

At the same time, the figure should not be interpreted as implying that exchange rates alone determine a country’s external position. Current account outcomes are also shaped by a broad range of structural and macroeconomic factors, including fiscal policy, domestic saving and investment behavior, demographic trends, productivity growth, commodity prices and global business cycles. The dispersion of observations around the fitted regression line reflects the influence of these additional forces.

Nevertheless, the overall pattern suggests that exchange-rate movements remain an important component of the external adjustment process. Across more than two decades of observations and diverse economic structures, countries experiencing relatively stronger real exchange rates generally record weaker current account positions, while those with relatively weaker exchange rates tend to exhibit stronger external balances. The consistency of this relationship provides empirical support for the broader argument developed in this article: Exchange-rate adjustment continues to play a meaningful role in correcting persistent global imbalances and should remain an integral element of international macroeconomic policy discussions.

These arguments have been advanced in recent policy discussions emphasizing the need for coordinated appreciation of Asian currencies as part of a broader global adjustment strategy.

Coordinated currency intervention should once again become an integral component of international macroeconomic policy. Rather than viewing exchange-rate adjustment as a passive consequence of domestic reforms, policymakers should recognize exchange-rate realignment as an active catalyst for structural transformation. Exchange rates alter relative prices immediately, influence trade incentives, reshape investment decisions and generate political momentum for domestic reforms that might otherwise remain politically unattainable.

The central thesis advanced here is that coordinated appreciation of Asian surplus-country currencies represents the most economically efficient and politically feasible mechanism for reducing global imbalances while avoiding the destructive consequences of escalating protectionism. Such coordination would not eliminate the need for domestic reforms. Instead, it would create conditions under which reforms become more effective and politically sustainable.

Beyond supporting renewed currency diplomacy, this article proposes a broader institutional framework that may be described as Strategic Coordinated Currency Realignment (SCCR). Unlike the Plaza Accord, which focused primarily on exchange-rate adjustments among advanced economies, SCCR would integrate exchange-rate coordination with macroeconomic policy consultation, digital financial infrastructure, reserve transparency and multilateral surveillance. It would therefore represent not merely an exchange-rate agreement but a comprehensive architecture for managing systemic imbalances in a multipolar monetary system.

Why exchange rates still matter

One of the most significant shifts in international macroeconomic thinking over the past 20 years has been the diminished emphasis placed on exchange rates as instruments of external adjustment. Contemporary policy discussions frequently argue that current-account balances are primarily determined by national saving-investment gaps, demographic trends, fiscal policies and structural characteristics of domestic economies. Exchange-rate movements, according to this perspective, merely reflect these underlying fundamentals.

Although this framework captures important long-run relationships, it tends to underestimate the independent influence of exchange-rate movements on trade behavior. Relative prices remain fundamental determinants of international competitiveness. Exchange-rate adjustments alter export profitability, import substitution, corporate investment decisions and production location choices almost immediately, whereas structural reforms often require many years before measurable effects emerge.

Historical experience provides substantial evidence supporting this proposition. The Plaza Accord did not eliminate US trade deficits overnight, but it significantly altered the trajectory of international trade over subsequent years. The substantial depreciation of the US dollar contributed to improved American export competitiveness and a gradual reduction in bilateral trade imbalances, particularly with Japan. While fiscal consolidation and domestic reforms undoubtedly contributed to adjustment, exchange-rate realignment served as the initial catalyst that shifted relative prices throughout the global economy. Recent discussions emphasizing the historical significance of the Plaza Accord similarly argue that its contribution has been underestimated in contemporary policy debates.

Moreover, empirical evidence consistently demonstrates that nominal exchange-rate changes translate into real exchange-rate adjustments because domestic prices adjust only gradually. Price rigidities imply that currency appreciation or depreciation affects competitiveness over extended periods before inflation differentials fully offset nominal movements. Consequently, exchange-rate policy retains considerable macroeconomic significance despite increasing globalization of production networks.

This insight has important implications for current policy debates. Many international organizations implicitly assume that exchange-rate movements should follow structural reforms rather than precede them. Such sequencing may unnecessarily delay adjustment. A coordinated appreciation of surplus-country currencies can immediately alter incentives facing exporters, investors and consumers. Governments subsequently face stronger incentives to implement domestic policies that support internal demand, productivity growth and economic diversification.

Exchange rates therefore should not be viewed as passive indicators reflecting deeper economic fundamentals. They are policy variables capable of influencing those fundamentals themselves. Recognizing this dynamic relationship constitutes the first step toward restoring currency diplomacy as an effective instrument of international economic cooperation.

The structural origins of contemporary global imbalances

Global trade imbalances are neither accidental nor solely the product of market forces. They reflect the interaction of macroeconomic policies, institutional structures, demographic trends, financial systems and exchange-rate management. While every current-account surplus corresponds mechanically to another country’s deficit, the persistence of these imbalances over several decades suggests that adjustment mechanisms within the international monetary system have become increasingly ineffective.

Since the Global Financial Crisis, East Asia has become the principal source of global current-account surpluses. China remains the largest contributor in absolute terms, while Japan, South Korea, Taiwan and several Association of Southeast Asian Nations (ASEAN) economies continue to generate sizeable external surpluses through different economic models. Japan’s surplus increasingly reflects investment income from its extensive overseas assets, whereas Korea and Taiwan continue to maintain exceptionally competitive manufacturing export sectors, particularly in semiconductors, electronics, automobiles and advanced industrial technologies.

These developments have occurred alongside relatively weak currencies in real effective exchange-rate terms, reinforcing export competitiveness over extended periods. Recent policy analyses emphasize that the combination of persistent surpluses and undervalued currencies has become a defining characteristic of East Asia’s external position.

Conversely, the US has continued to operate as the world’s principal consumer of last resort. Large fiscal deficits, deep and highly liquid capital markets, and the dollar’s reserve-currency status have enabled the US to sustain persistent current-account deficits without facing the financing constraints that would normally affect other economies. Capital inflows generated by foreign reserve accumulation have reduced borrowing costs, encouraged domestic consumption and reinforced America’s role as the destination for excess global savings.

This asymmetry has produced what economists have long described as a “global savings glut.” Yet the term may now understate the broader structural problem. The issue is no longer merely excessive savings; rather, it is the geographical concentration of those savings in economies pursuing export-oriented development strategies that suppress domestic consumption relative to output.

China illustrates this dynamic particularly clearly. Although considerable progress has been made in expanding household income and developing domestic consumption, investment and exports continue to play disproportionately important roles in economic growth. Local governments, state-owned enterprises and policy-directed financial institutions have historically prioritized industrial expansion and export competitiveness. The resulting production capacity frequently exceeds domestic demand, encouraging firms to seek external markets.

The interaction between industrial policy and exchange-rate management further complicates adjustment. Modern industrial policy is not limited to subsidies or preferential financing. It increasingly incorporates exchange-rate policies, sovereign wealth fund operations, public-sector foreign-asset accumulation, export credit institutions and state-directed investment. Distinguishing between “micro” industrial policy and ”macro” exchange-rate policy therefore becomes increasingly difficult in practice. Recent critiques of existing IMF frameworks similarly argue that these interactions remain inadequately captured within conventional external-balance assessments.

Another important contributor to persistent imbalances has been the accumulation of official foreign-exchange reserves. During the two decades preceding the Global Financial Crisis, Asian central banks accumulated unprecedented quantities of dollar-denominated assets. Such reserve accumulation simultaneously prevented domestic currencies from appreciating and generated sustained demand for US Treasury securities. Rather than reflecting purely market-driven capital flows, a substantial proportion of global financial integration was mediated through official institutions pursuing exchange-rate objectives.

This historical perspective challenges the widely held belief that financial globalization naturally produces equilibrium exchange rates. Official intervention has repeatedly altered market outcomes by influencing both capital flows and currency values. Ignoring these interventions risks misunderstanding the persistence of global imbalances.

The limitations of unilateral adjustment

If exchange-rate misalignments contribute significantly to persistent external imbalances, why have governments not pursued more active currency adjustments? The answer lies primarily in political economy.

Currency appreciation generates concentrated costs while distributing benefits more broadly. Export-oriented industries immediately experience declining international competitiveness, reduced profit margins and pressure on employment. By contrast, the benefits of appreciation — higher purchasing power, lower import prices, improved resource allocation and stronger real incomes — emerge gradually and are dispersed across households and firms.

This asymmetry creates a classic collective-action problem. Every surplus economy recognizes the long-term benefits of reducing external dependence, yet no government wishes to become the first mover. The first country to appreciate its currency risks losing export market share to neighboring economies maintaining weaker exchange rates.

This first-mover disadvantage explains why unilateral appreciation rarely occurs voluntarily. Even when policymakers recognize that stronger currencies would ultimately improve domestic economic welfare, immediate political costs often outweigh longer-term gains.

Protectionist responses in deficit countries produce an equally problematic outcome. Tariffs alter bilateral trade patterns but seldom reduce aggregate external imbalances. Instead, production relocates geographically, supply chains reorganize and trade flows are redirected through third countries. Recent years have demonstrated that tariffs imposed on Chinese exports have frequently encouraged production shifts toward Southeast Asia rather than substantially reducing America’s overall trade deficit.

Financial sanctions similarly possess important geopolitical functions but cannot substitute for macroeconomic adjustment. Sanctions influence specific transactions, institutions or countries; they do not systematically address underlying saving-investment imbalances across the global economy.

Recent policy discussions within the US have increasingly recognized these limitations. Stephen Miran, a former Federal Reserve Board of Governors, argues that tariffs should be understood as one component of a broader strategy to restructure the international trading system, rather than as a stand-alone solution. In his framework, durable external adjustment may also require exchange-rate policy and, where feasible, multilateral currency coordination to address the underlying macroeconomic sources of persistent trade imbalances.

Consequently, the international system finds itself trapped between two ineffective adjustment mechanisms. Surplus countries hesitate to appreciate their currencies individually, while deficit countries increasingly rely upon tariffs, industrial subsidies, export controls and national security measures. Neither strategy resolves the underlying macroeconomic disequilibrium.

As US Treasury Secretary Scott Bessent argued, the objective is not simply to impose tariffs but to “rebalance the international economic system.” Because international trade, finance and security constitute “a web of relationships” that “cannot [be taken] in isolation,” exchange-rate policy, industrial policy and trade policy should likewise be viewed as complementary instruments rather than independent policy domains.

The logic of coordinated intervention directly addresses this coordination failure. If major surplus economies appreciate simultaneously, none suffers a disproportionate competitive disadvantage. Export competitiveness adjusts collectively rather than individually. Political resistance diminishes because adjustment costs are shared across participants.

From a game-theoretic perspective, coordinated appreciation transforms what would otherwise resemble a prisoner’s dilemma into a cooperative equilibrium. Mutual participation becomes individually rational because no participant bears the burden of adjustment alone. This logic constituted one of the principal strengths of the Plaza Accord in 1985 and remains equally relevant today.

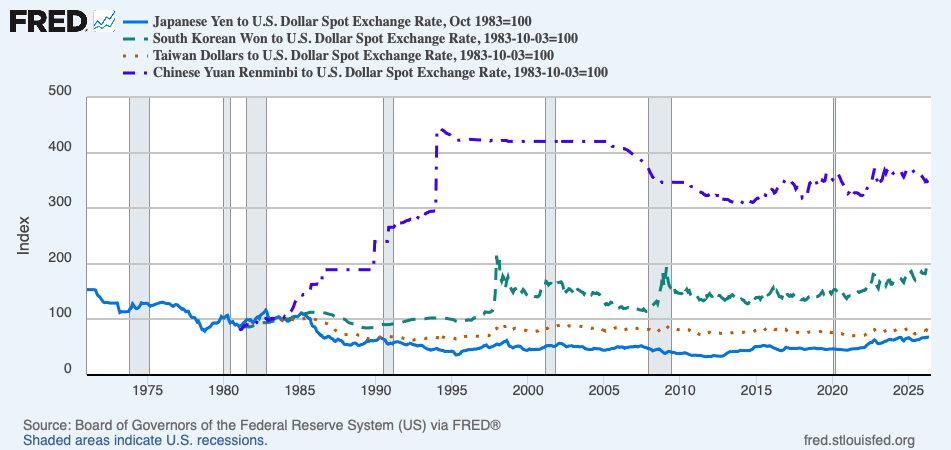

Figure 3 illustrates the evolution of the major East Asian currencies against the US dollar since the Plaza Accord. Although the Japanese yen appreciated sharply following the 1985 agreement, subsequent exchange-rate movements across Asia have been considerably more heterogeneous. The renminbi remained tightly managed for much of the period, while the Korean won and Taiwan dollar experienced more gradual adjustments. The figure demonstrates that coordinated appreciation has not been sustained across the region, helping to explain the persistence of external imbalances discussed in the preceding sections.

The challenge is not whether coordinated appreciation can influence trade balances; historical evidence suggests that it can. The challenge lies in designing institutions capable of generating sufficient political commitment among participating economies under far more complex geopolitical circumstances than existed four decades ago.

Strategic coordinated currency realignment

The debate over exchange-rate coordination has long remained imprisoned by historical analogy. Whenever policymakers discuss coordinated intervention, comparisons with the Plaza Accord inevitably dominate the conversation. Such comparisons are understandable but ultimately misleading. The international monetary system that emerged during the 1980s was organized around a relatively small group of advanced industrial democracies operating under American monetary leadership. Capital mobility, although expanding rapidly, remained substantially lower than it is today; global supply chains were considerably less integrated; and China had yet to emerge as a central actor in international production and finance. Attempting to replicate the Plaza Accord under contemporary conditions would therefore misunderstand both the transformation of the global economy and the changing nature of monetary power itself.

What is required is not a Second Plaza Accord in the historical sense but an entirely new architecture of international monetary cooperation. The central challenge confronting policymakers today is no longer the correction of a single overvalued reserve currency. Rather, it is the management of persistent structural imbalances generated by asymmetries in domestic demand, reserve accumulation, industrial policy and exchange-rate management across multiple major economies. These imbalances are increasingly reinforced by geopolitical fragmentation, technological competition and the emergence of new digital payment infrastructures. Exchange-rate coordination, therefore, can no longer be conceived as an isolated monetary instrument. It must become part of a broader framework that integrates macroeconomic policy coordination, financial governance and strategic diplomacy.

This article proposes such a framework under the concept of SCCR. The framework differs fundamentally from previous models of international monetary cooperation because it treats exchange-rate adjustment not as the ultimate objective of coordination but as the mechanism through which broader macroeconomic rebalancing can be initiated.

Conventional policy discussions frequently assume that structural reforms must precede currency adjustment. According to this view, countries should first reform labor markets, expand domestic demand, improve fiscal sustainability or liberalize financial systems before exchange rates can adjust sustainably. While theoretically appealing, such sequencing has repeatedly produced policy paralysis. Structural reforms are politically costly, their benefits are delayed and governments facing little immediate economic pressure possess few incentives to undertake them.

Exchange-rate adjustment, by contrast, alters economic incentives almost instantaneously. Relative prices change immediately, export profitability is recalculated overnight, import substitution becomes less attractive and firms begin reallocating investment toward productivity enhancement rather than exchange-rate arbitrage. In this sense, currency realignment should not be regarded as the consequence of successful reform but as one of its principal catalysts.

Recent proposals advocating coordinated appreciation of major Asian currencies correctly recognize this sequencing problem. Rather than waiting indefinitely for domestic reforms in surplus economies or for fiscal consolidation in deficit economies, coordinated appreciation could initiate the adjustment process itself by reshaping incentives facing producers, consumers and investors simultaneously. Yet even these proposals remain largely confined to the traditional language of exchange-rate policy. Their broader significance lies elsewhere. Coordinated intervention should be understood as a mechanism for restoring confidence in multilateral economic governance at a time when international cooperation has become increasingly fragmented.

The political economy of unilateral appreciation illustrates why coordination is indispensable. Every surplus economy recognizes that excessive dependence upon external demand ultimately constrains domestic welfare by suppressing household consumption and encouraging overinvestment in export sectors. Yet no government wishes to appreciate first.

The immediate political costs are concentrated among influential exporting industries, while the benefits — higher real wages, stronger purchasing power, lower imported inflation and more balanced economic growth — are dispersed across the broader population and materialize only gradually. Consequently, every government rationally delays adjustment while hoping that others move first. The resulting equilibrium resembles a classic coordination failure rather than an efficient market outcome.

Coordinated intervention fundamentally changes these incentives. Simultaneous appreciation distributes adjustment costs across competing export economies, thereby eliminating the first-mover disadvantage that has historically discouraged reform. Manufacturers compete under relatively unchanged regional exchange-rate relationships, while all participants collectively contribute to reducing global imbalances. This is not an attempt to manipulate markets but rather an effort to restore market signals that have been persistently distorted by prolonged official intervention, reserve accumulation and policy asymmetries.

Digital finance and monetary leadership

The argument becomes even more compelling when viewed through the lens of international political economy. Exchange rates have never been purely technical variables. They embody strategic choices regarding the distribution of global demand, the allocation of industrial production, and the balance between domestic welfare and external competitiveness.

Throughout modern history, reserve currencies have derived their international status not merely from economic size but from institutional credibility, financial openness, legal stability and geopolitical leadership. Contemporary debates concerning digital currencies, stablecoins and central bank digital currencies reinforce rather than diminish this conclusion.

Technological innovation may transform payment mechanisms, settlement systems and financial intermediation, but it cannot substitute for the institutional foundations upon which international monetary confidence ultimately depends. Recent discussions among monetary scholars similarly conclude that payment technologies are likely to complement rather than displace the traditional determinants of reserve-currency status.

This observation carries an important implication for international monetary reform. Much contemporary discussion has focused on whether digital currencies will challenge dollar dominance. Such questions, while intellectually interesting, risk overlooking a more fundamental issue. The principal weakness of the existing monetary order is not technological obsolescence but institutional fragmentation. Cross-border payment systems may become faster, cheaper and more decentralized, yet none of these innovations can resolve persistent current-account imbalances or substitute for coordinated macroeconomic adjustment. Monetary technology changes the speed at which transactions occur; it does not determine whether global demand is sustainably distributed across economies.

Much contemporary discussion has focused on whether digital currencies will challenge the dominance of the US dollar. Such debates, while intellectually appealing, often overlook a more fundamental issue. The principal weakness of the current international monetary system is not technological obsolescence but institutional fragmentation. Faster payment systems and digital settlement technologies may improve the efficiency of cross-border transactions, yet they cannot by themselves resolve persistent current-account imbalances or substitute for coordinated macroeconomic adjustment.

This perspective is increasingly reflected in official US policy. Upon the signing of the GENIUS Act, Bessent announced that stablecoins would strengthen rather than weaken the international role of the dollar, describing them as an “internet-native payment rail” capable of expanding global access to dollar-denominated transactions while reinforcing demand for US Treasury securities. In his view, digital financial innovation would enhance the foundations of dollar leadership rather than replace them.

Bessent’s observation reinforces a broader point. Technological innovation can transform the speed, efficiency and accessibility of international payments, but it cannot substitute for the institutional foundations upon which reserve-currency status ultimately depends. Financial depth, legal certainty, policy credibility and international confidence remain the essential pillars of monetary leadership. Digital technologies therefore complement existing monetary institutions rather than fundamentally replacing them.

Against this background, SCCR conceives digital financial innovation as enabling infrastructure rather than an independent source of monetary transformation. Central bank digital currencies, tokenized deposits, interoperable payment systems and regulated stablecoins should facilitate greater transparency and lower transaction costs while operating within a framework of coordinated macroeconomic and exchange-rate policies. Without such coordination, technological innovation may accelerate financial flows, but it cannot correct the structural imbalances that continue to undermine the stability of the international monetary system.

SCCR therefore conceives digital financial innovation as an enabling infrastructure rather than an independent source of monetary transformation. Central bank digital currencies, tokenized deposits, interoperable payment systems and regulated stablecoins should facilitate greater transparency and lower transaction costs while operating within an internationally coordinated macroeconomic framework. Absent such coordination, technological innovation merely accelerates financial flows without correcting the structural imbalances that generate instability in the first place.

Restoring currency diplomacy

Perhaps the greatest contribution of SCCR lies in redefining currency diplomacy itself. For much of the post-Cold War era, international monetary cooperation has gradually retreated from the center of economic diplomacy. Exchange rates have been treated either as matters of domestic monetary policy or as outcomes best left entirely to financial markets. Simultaneously, governments have increasingly relied upon tariffs, industrial subsidies, export controls, investment restrictions and financial sanctions to pursue strategic objectives. The result has been the progressive securitization of international economic policy. Trade policy has become geopolitical policy, while exchange-rate diplomacy has largely disappeared from the international agenda.

This evolution represents a profound strategic mistake. Tariffs alter trade patterns but rarely eliminate aggregate imbalances. Industrial subsidies encourage retaliatory intervention. Financial sanctions fragment global capital markets while encouraging the development of parallel payment systems. None addresses the underlying macroeconomic asymmetries that continuously regenerate external disequilibria.

Exchange-rate coordination, by contrast, operates through relative prices rather than administrative restrictions. It preserves market allocation while correcting distortions that markets alone have proven unable to eliminate. Properly designed, coordinated intervention should therefore be understood not as an alternative to market capitalism but as an instrument for preserving its long-run stability.

In this respect, Strategic Coordinated Currency Realignment should be viewed as a 21st-century framework for managing interdependence rather than constraining it. Its objective is neither fixed exchange rates nor permanent intervention. Instead, it seeks to restore exchange rates to their appropriate role as equilibrating mechanisms within a cooperative international monetary system. By integrating exchange-rate coordination with macroeconomic consultation, institutional transparency and digital financial governance, SCCR offers a more comprehensive and strategically coherent vision of international monetary cooperation than has existed since the collapse of the Bretton Woods system.

The geopolitical economy of currency realignment

The strategic importance of coordinated currency appreciation extends well beyond macroeconomic stabilization. In the contemporary international system, exchange-rate policy has become inseparable from questions of geopolitical influence, technological competition and the future architecture of globalization itself. The international monetary order is no longer merely a mechanism for facilitating cross-border transactions; it has become a central arena in which states compete for economic security, industrial leadership and strategic autonomy. Consequently, any discussion of coordinated intervention must be situated within this broader geopolitical transformation.

Much of the current debate has focused on whether the international monetary system is entering a period of de-dollarization. This narrative, while politically attractive, often oversimplifies the evolution of reserve currencies. Monetary history demonstrates that reserve currencies rarely disappear abruptly. Instead, international monetary transitions typically unfold over several decades as economic power, financial depth, institutional credibility and geopolitical leadership gradually redistribute across major economies.

Sterling did not collapse when the US surpassed Britain economically, nor did the dollar immediately replace sterling after the Second World War. Extended periods of coexistence characterized both transitions, during which several currencies simultaneously fulfilled international functions. Recent discussions among monetary scholars similarly suggest that the dollar’s dominance is likely to erode gradually rather than disappear suddenly, provided credible alternatives continue to develop.

China’s monetary strategy and exchange-rate diplomacy

This historical perspective is particularly relevant when assessing China’s international monetary ambitions. Considerable attention has been devoted to the internationalization of the renminbi, frequently interpreted as an attempt to displace the dollar from its dominant international position. Such interpretations, however, may exaggerate both China’s immediate objectives and its current capabilities.

Despite substantial progress in cross-border settlement, bilateral trade invoicing and regional payment arrangements, the renminbi continues to account for only a modest share of global reserve holdings. Capital controls remain extensive, financial markets remain only partially open and the institutional characteristics traditionally associated with reserve currencies — judicial independence, transparent governance, unrestricted capital mobility and deep private financial markets — remain incomplete.

China’s monetary strategy therefore appears less directed toward replacing the dollar than toward reducing strategic vulnerability to it. The experience of financial sanctions imposed on Russia following its invasion of Ukraine reinforced concerns among Chinese policymakers regarding excessive dependence upon dollar-based payment networks and reserve assets. From this perspective, initiatives such as the Cross-Border Interbank Payment System (CIPS), expansion of renminbi-denominated trade settlement, bilateral currency swap arrangements and experimentation with central bank digital currency should be interpreted primarily as instruments of economic resilience rather than immediate challenges to dollar supremacy. Recent policy discussions similarly conclude that China’s objective is best understood as building monetary insurance against geopolitical disruption rather than seeking rapid replacement of the existing reserve-currency order.

This distinction has profound implications for exchange-rate diplomacy. If China’s objective is resilience rather than monetary hegemony, coordinated appreciation of Asian currencies becomes politically more plausible than commonly assumed. Participation in a multilateral appreciation framework would not require China to abandon its long-term strategic interests. On the contrary, a stronger renminbi could facilitate precisely the domestic economic transformation that Chinese policymakers have repeatedly identified as essential: reducing dependence upon investment- and export-led growth while strengthening household consumption as the principal engine of long-term development. Exchange-rate appreciation would therefore reinforce, rather than contradict, China’s own stated objective of achieving higher-quality economic growth.

Japan, the US and Europe’s strategic adjustment

Japan occupies an equally significant position within this evolving monetary landscape. For more than three decades, Japanese economic policy has often treated yen appreciation primarily as a macroeconomic challenge associated with declining export competitiveness and deflationary pressure. Yet this perspective increasingly understates Japan’s strategic advantages.

As demographic aging accelerates and labor-force constraints become more binding, long-term prosperity will depend less on maximizing export volumes than on raising productivity, capital efficiency, technological sophistication and real household income. A stronger yen, when accompanied by continued structural reform, should therefore be interpreted not as an economic liability but as a strategic asset. Currency appreciation enhances purchasing power, reduces imported inflation, encourages firms to innovate rather than compete through price alone and strengthens Japan’s role as a provider of international financial stability.

The implications extend beyond Asia. The US has increasingly relied on tariffs, industrial policy, export restrictions and investment screening as instruments to address trade imbalances and technological competition. While such policies may pursue legitimate national security objectives, they do not eliminate the macroeconomic conditions generating persistent external deficits. Indeed, excessive reliance upon protectionist instruments risks fragmenting global production networks while leaving underlying current-account imbalances largely unchanged.

Exchange-rate coordination offers a more durable adjustment mechanism because it addresses competitiveness through relative prices rather than administrative barriers. In this sense, coordinated intervention should not be viewed as an alternative to strategic competition but as a means of preventing strategic competition from degenerating into systemic economic fragmentation.

Europe likewise has a critical role to play. The EU has frequently found itself caught between American demand, Asian export competitiveness and its own relatively weak domestic investment performance. A more balanced international monetary order would reduce these external pressures by encouraging stronger domestic demand in surplus economies and more sustainable fiscal trajectories in deficit economies.

Simultaneously, deeper European capital markets and greater investment in productivity-enhancing sectors would strengthen the euro’s international role within an increasingly multipolar monetary system. Multipolarity, properly understood, should not be interpreted as rivalry among reserve currencies but as diversification of global monetary resilience.

Toward a new currency diplomacy

This broader perspective reveals why coordinated currency intervention should no longer be viewed as a narrow technical question for finance ministries and central banks. Exchange-rate policy has become an essential component of grand strategy. It influences industrial competitiveness, technological investment, geopolitical alliances, financial stability and the future distribution of international economic leadership. The contemporary international monetary system therefore requires a new form of currency diplomacy — one that recognizes exchange rates not merely as prices determined in foreign-exchange markets but as strategic variables shaping the evolution of the global political economy itself.

Ultimately, the greatest risk confronting the international monetary system is not the gradual emergence of monetary multipolarity. History suggests that diversified reserve systems can function effectively when supported by robust institutions and cooperative governance. The greater danger lies in allowing persistent macroeconomic imbalances to be addressed primarily through unilateral protectionism, financial coercion and competitive industrial policy. Such a trajectory would gradually replace the rules-based international economic order with competing regional blocs, diminishing global efficiency while increasing geopolitical instability.

SCCR offers a practical framework for preserving and strengthening an open, rules-based international economic system by addressing the persistent structural imbalances that have contributed to protectionism, geopolitical fragmentation and financial instability. Rather than weakening the international role of the US dollar, SCCR seeks to reinforce the institutional foundations that have long underpinned dollar leadership while facilitating a more balanced distribution of global demand. Through coordinated exchange-rate adjustment, credible domestic reforms, institutional transparency and digital financial cooperation, SCCR provides a realistic pathway toward a more stable, resilient and genuinely multipolar international monetary order.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

The Problem with the Dollar: When One Nation’s Currency Becomes the World’s

The US dollar serves as both the world’s reserve currency and America’s national currency, forcing other countries to accumulate dollars...

In Trade Rivalry With the US, China Will Not Become Another Japan

China, which enjoys a hefty trade surplus vis-à-vis the US, is paying attention to history. Back in the 1980s, a...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

The Truth About Central Bank Digital Currency: It’s Indispensable

Many observers are suspicious of Federal Reserve-issued digital currency. They see it as a way for government to extend its...

Comment