For more than three decades, Japan has occupied a unique position in global aviation finance. Through Japanese Operating Leases (JOLs) and Japanese Operating Leases with Call Options (JOLCOs), Japanese investors have supplied billions of dollars in equity capital to airlines worldwide. At its peak, annual JOLCO issuance exceeded ¥1 trillion (approximately $7–10 billion), and Japanese investors accounted for an estimated 20–30% of global aircraft lease-equity funding. Alongside Ireland’s leasing ecosystem and, more recently, China’s state-backed financiers, Japan became one of the most important sources of aviation capital globally.

The model appeared remarkably successful. Airlines obtained aircraft with limited upfront capital commitments. Japanese investors received attractive tax-adjusted returns, often in the range of 5–8% after accounting for depreciation benefits. Banks generated stable lending income secured by globally mobile assets. The interests of airlines, investors and lenders appeared aligned.

Today, however, the foundations of that model are weakening.

Industry participants often attribute current difficulties to cyclical headwinds: higher interest rates, a weaker yen, delayed aircraft deliveries and temporary turbulence in airline profitability. Yet such explanations risk missing the larger story. The more consequential challenge is structural. A combination of accounting reforms, evolving tax policy, tighter regulation, shifting investor preferences and changing capital-market conditions has steadily eroded the advantages that once made Japanese aircraft-leasing structures uniquely attractive.

Moreover, the international tax environment has become significantly more complex. Japanese investors must increasingly consider cross-border tax issues arising from the OECD’s Base Erosion and Profit Shifting (BEPS) initiative, the global minimum tax framework and evolving international tax rules. As these developments affect the economic assumptions underlying JOL and JOLCO transactions, a growing challenge lies in whether domestic leasing companies and trading houses — the principal arrangers of such structures — can adequately explain and manage these risks for investors. Insufficient understanding of international tax exposure may itself become a material risk factor for the market.

The question is no longer whether JOLCO survives. The question is whether a model designed for the financial environment of the late 20th century can remain competitive in the 21st.

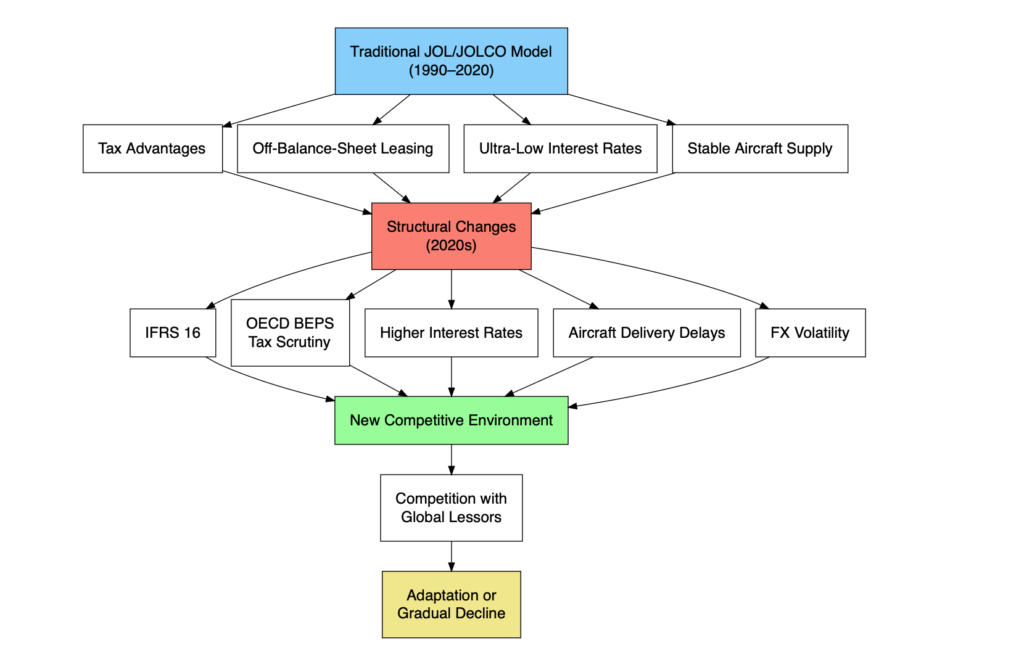

The three pillars of success

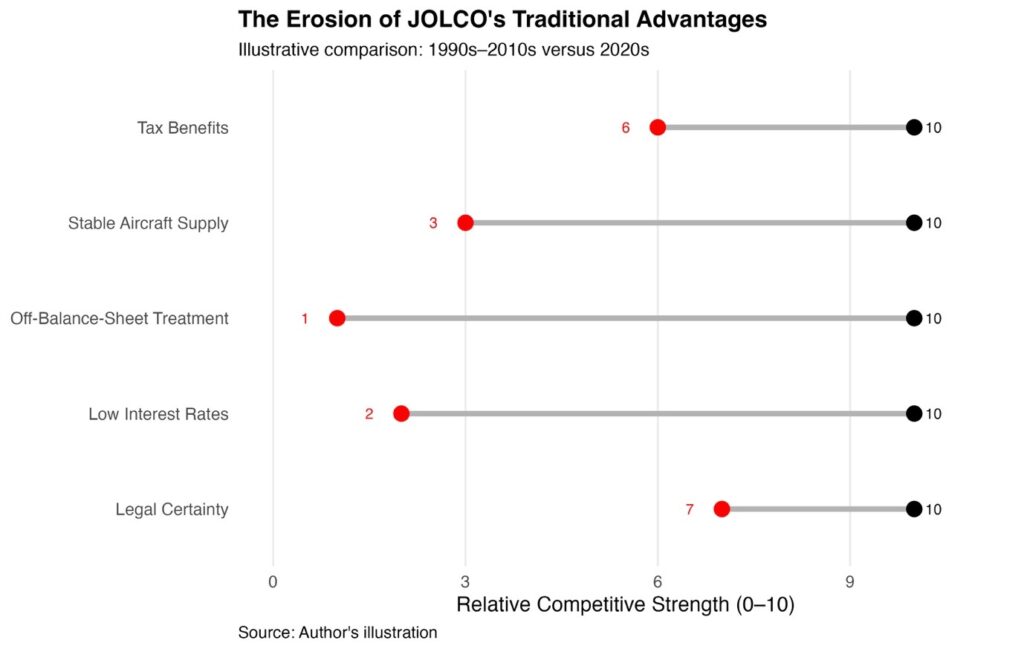

Historically, JOL and JOLCO transactions rested on three powerful advantages. The first was tax efficiency. Accelerated depreciation and interest deductions allowed investors to reduce taxable income while generating attractive after-tax returns. The second was accounting treatment. Airlines could lease aircraft while avoiding much of the balance-sheet impact associated with ownership or conventional debt financing. The third was predictability. Aircraft values, lease cash flows and funding costs remained relatively stable throughout much of the 1990s and 2000s.

Together, these factors created a powerful ecosystem. A typical JOLCO transaction involved 20–30% equity and 70–80% debt financing. During the era of ultra-low interest rates, leverage amplified returns while depreciation enhanced investor economics.

Today, all three pillars are under pressure.

The end of off-balance-sheet leasing

Perhaps the most significant change has been accounting reform.

For decades, global airlines viewed operating leases as an attractive means of financing aircraft because lease obligations remained largely off balance sheet. That advantage largely disappeared with the introduction of International Financial Reporting Standards (IFRS) 16 by the International Accounting Standards Board (IASB). Under the new standard, most leases must be recognized through right-of-use assets and corresponding lease liabilities.

The impact has been substantial. According to the International Air Transport Association (IATA), IFRS 16 added approximately $500 billion of lease liabilities to airline balance sheets worldwide.

Japan is moving in the same direction. The Accounting Standards Board of Japan (ASBJ) Lease Accounting Reform aligns Japanese accounting treatment more closely with international standards.

The implications are straightforward. Airlines can no longer justify operating leases primarily on accounting grounds. Instead, leasing decisions increasingly depend on actual economics: financing costs, operational flexibility, fleet strategy and liquidity management.

As a result, JOLCO structures now compete directly with bank loans, export-credit facilities, enhanced equipment trust certificates (EETCs), and large global lessors such as AerCap, SMBC Aviation Capital and Avolon.

As a result, one of the principal historical attractions of JOLCO structures — the ability to improve reported leverage through off-balance-sheet treatment — has largely vanished.

At the same time, the investor base that has traditionally supported JOLCO transactions may also be narrowing. Many Japanese investors participate through relatively small equity commitments rather than funding entire aircraft. As economic conditions become more challenging and domestic businesses face greater cash-flow pressure, these investors may become less willing or able to allocate capital to aircraft-leasing investments. This could gradually shift the market toward a smaller pool of more sophisticated and professional investors.

While such a transition may improve investment discipline and due diligence, it could also reduce transaction volumes and place pressure on the existing business models of leasing companies and trading houses that rely on a broad retail and middle-market investor base. Maintaining current staffing levels and fee structures may become increasingly difficult in a more concentrated market.

A business model dependent on tax policy

If accounting arbitrage has diminished, tax efficiency remains central to the economics of many JOLCO transactions. This dependence creates a structural vulnerability.

Although JOLCO is often presented as an aviation investment, many participants have historically been motivated less by aircraft economics than by tax benefits. Accelerated depreciation and interest deductibility frequently constitute a significant share of expected returns.

Aircraft leases typically extend for eight to 12 years, while aircraft themselves remain in service for 25 years or more. Tax policy, by contrast, can change within a single budget cycle.

Over the past decade, OECD-led BEPS initiatives have encouraged governments to tighten rules governing tax-driven investment structures. Japan has gradually strengthened earnings-stripping regulations and anti-avoidance provisions. The framework is summarized by the National Tax Agency of Japan’s Earnings-Stripping Rules.

The risk is not prohibition. The risk is uncertainty. A structure whose economics depend heavily on favorable tax treatment becomes inherently fragile when that treatment is subject to political or regulatory reinterpretation.

Unlike Ireland’s leasing industry — which benefits from scale, operational expertise, treaty networks and diversified funding sources — Japan’s leasing model remains unusually dependent on the continuation of specific tax advantages.

The end of free money

The rise of JOLCO coincided with one of the most extraordinary monetary-policy environments in modern history.

Many investors entering the market today are also part of a generational transition. Unlike earlier participants who experienced periods of higher inflation and interest rates, a large share of Japanese investors built their investment expectations during an era of ultra-low borrowing costs and abundant liquidity. As a result, they are entering a market environment that is fundamentally different from the one in which JOLCO structures originally flourished.

This shift makes a deeper understanding of both the benefits and the risks of aircraft leasing increasingly important. Once committed, investors are typically locked into transactions for four to 12 years, limiting their flexibility and requiring assumptions about future interest rates, tax rules, aircraft values and airline creditworthiness over a long horizon. In an environment characterized by greater economic uncertainty, such long-term forecasting has become considerably more difficult.

Between 2010 and 2021, Japanese interest rates remained near zero, while global borrowing costs reached historic lows. Such conditions were highly favorable for leveraged investment structures.

Aircraft leasing is particularly sensitive to financing costs because debt typically finances 60–80% of acquisition value. Consider a $100 million aircraft financed with 70% debt. A one-percentage-point increase in borrowing costs reduces annual cash flow by approximately $700,000. Over a ten-year lease term, the cumulative impact can exceed $7 million even before considering any refinancing costs or changes in future credit conditions.

Since 2022, benchmark interest rates in major economies have risen by roughly 500 basis points. The shift is documented extensively in the Bank for International Settlements Annual Economic Report 2024.

Even if policy rates decline, few investors expect a return to the near-zero funding environment that characterized the previous decade. The economics of leveraged aircraft leasing have therefore changed fundamentally.

Delivery delays have become a systemic risk

Aviation finance has traditionally focused on airline creditworthiness and aircraft residual values. Today, operational risk may be more important.

Both Airbus and Boeing continue to face production constraints and supply-chain disruptions. Airbus delivered 766 aircraft in 2024 but has repeatedly warned of bottlenecks affecting engines, avionics and structural components. The company’s outlook is outlined in its Aircraft Production Ramp-Up Strategy.

Boeing’s challenges have been even more severe following manufacturing-quality concerns and regulatory intervention. A detailed assessment is available in Reuters’ analysis of Boeing’s 2024 crisis.

For airlines, delivery delays are frustrating. For JOLCO structures, they can be destabilizing. Aircraft-financing transactions depend on precise coordination between equity subscriptions, debt drawdowns, lease commencement, foreign-exchange hedging and tax recognition. When deliveries are delayed by months or years, financing commitments expire, hedges become ineffective and transaction documents require renegotiation.

Large lessors managing portfolios of hundreds of aircraft can absorb such disruptions. Single-aircraft special-purpose vehicles cannot.

Legal certainty is no longer assumed

Aircraft leasing has long been regarded as a legally robust asset class. Recent litigation has challenged that assumption.

Particular attention has been paid to termination-payment provisions frequently embedded in JOLCO transactions. Although English courts have generally upheld such provisions, litigation has highlighted a broader reality: Recovery outcomes depend on contractual drafting, jurisdictional interpretation and insolvency frameworks.

Detailed analyses are available from both Clifford Chance’s JOLCO Termination Sum Review and Morgan Lewis’ English High Court Analysis. For investors, the significance lies less in individual court decisions than in the uncertainty they reveal. Recovery values cannot simply be assumed; they must be analyzed.

This issue is particularly important in the Japanese market, where investor discussions have traditionally focused on tax benefits, projected returns and aircraft residual values rather than legal-enforcement risks. Many investors have limited experience evaluating complex cross-border insolvency proceedings, jurisdictional conflicts or contractual enforcement risks. As a result, legal risk is often treated as a secondary consideration despite its potential impact on recovery outcomes.

The challenge is compounded by the highly specialized nature of aircraft-finance disputes. While transaction documentation is typically prepared by experienced legal counsel, the practical outcome of a distressed lease often depends on litigation, restructuring negotiations and insolvency proceedings conducted across multiple jurisdictions. These factors can be difficult for non-professional investors to assess and are not always fully reflected in traditional investment presentations.

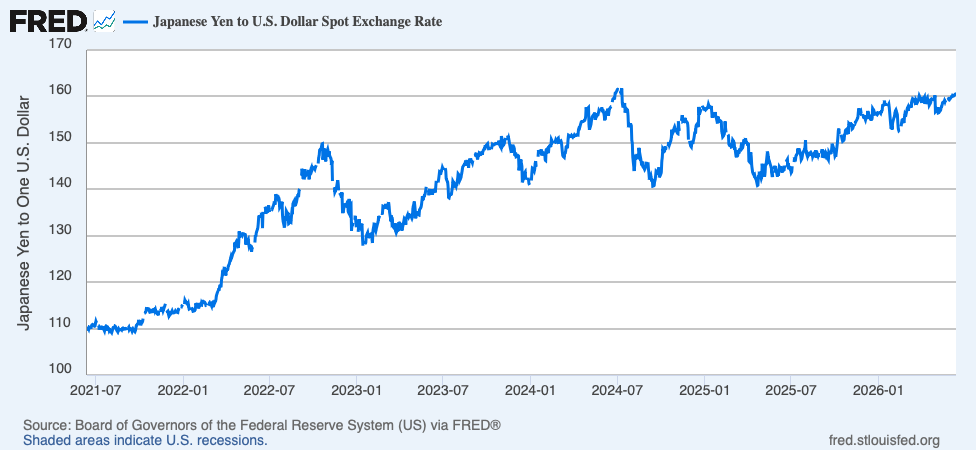

Currency risk has become more punitive

Currency exposure has also become increasingly significant. Aircraft are priced globally in US dollars, while Japanese investors provide capital largely in yen.

The yen depreciated from approximately ¥103 per dollar in early 2021 to nearly ¥160 per dollar during 2024. As a result, the yen cost of acquiring a $100 million aircraft increased from roughly ¥10.3 billion to ¥16 billion — an increase exceeding 50%. In our view, the recent weakness of the Japanese yen has materially reduced the attractiveness of dollar-denominated aircraft investments for many Japanese investors. The sharp depreciation of the yen has significantly increased the domestic-currency cost of acquiring aircraft, while higher hedging costs and greater exchange-rate uncertainty have further reduced expected risk-adjusted returns.

While hedging strategies can mitigate some exposure, long-dated currency protection remains expensive and imperfect. For many investors, foreign-exchange volatility now represents a greater source of uncertainty than aircraft performance itself.

Why insurance companies are looking elsewhere

These structural weaknesses become particularly apparent when viewed through the lens of insurance companies.

Japanese life insurers collectively manage assets exceeding ¥400 trillion. Yet JOLCO remains largely absent from their strategic asset allocations. The reason is straightforward. Insurance companies are not tax-driven investors. Their objective is to generate predictable long-duration cash flows while minimizing regulatory capital consumption. JOLCO performs poorly on both measures.

The structures involve airline credit risk, residual value uncertainty, legal enforcement complexity, delivery delays and opaque valuations. Under emerging solvency frameworks, including Japan’s Economic Value-Based Solvency Regulation (ESR), such characteristics attract relatively high capital charges.

Consequently, institutional participation remains limited despite the industry’s long history.

This limitation is unlikely to disappear in the future. Publicly listed companies and institutional investors face increasing scrutiny regarding tax planning, governance and capital allocation. As a result, participation in aircraft-leasing structures primarily motivated by tax benefits is becoming more difficult to justify. Rather than investing through traditional JOLCO arrangements, professional investors may prefer direct ownership stakes in aircraft-leasing companies, dedicated aviation-investment platforms or strategic acquisitions that provide greater control, transparency and scale. The trend suggests that future participation may become concentrated among a smaller number of sophisticated investors rather than the broad base of tax-oriented investors that historically supported the market.

A broader question of capital allocation

The deeper issue extends beyond aviation finance.

Historically, JOLCO has been marketed primarily to profitable, privately held companies, including owner-managed firms in construction, real estate, healthcare, logistics and leisure industries. Industry presentations frequently acknowledge that tax benefits remain the primary attraction for many participants. A representative overview is provided in the Airline Economics JOL/JOLCO Market Presentation.

This raises broader questions about capital allocation within Japan. When capital flows into highly engineered structures because depreciation benefits enhance returns, investment decisions become increasingly detached from underlying productivity. Financial engineering begins to substitute for genuine value creation.

The result is a subtle but important distortion. Capital that might otherwise support innovation, digital transformation, productivity enhancement or wage growth is instead directed toward tax-efficient ownership structures tied to aircraft operating thousands of miles away.

Such behavior may be rational from the perspective of individual investors. It is less obvious that it is optimal from the perspective of the Japanese economy.

Adaptation rather than extinction

None of this implies that JOLCO will disappear.

The global commercial aircraft fleet is expected to expand from approximately 29,000 aircraft today to more than 47,000 by 2043. Boeing and Airbus together forecast demand for more than 40,000 new aircraft over the next two decades, representing trillions of dollars of financing requirements.

There will continue to be opportunities for Japanese capital. But the conditions that once supported JOLCO’s rapid expansion — off-balance-sheet treatment, abundant tax advantages, ultra-low interest rates, stable supply chains and limited competition — have largely vanished. The challenge confronting Japan’s aircraft-leasing industry is therefore not one of survival but reinvention.

The next phase of global aviation finance will reward scale, operational expertise, capital efficiency and economic substance rather than tax optimization and financial engineering. Whether JOL and JOLCO can successfully adapt to that reality may determine their relevance in global aviation finance for the next generation.

The era in which Japanese aircraft leasing thrived because of accounting advantages, tax benefits and cheap money is drawing to a close. The industry’s future will depend on whether it can compete on economic merit alone. That may prove a far more demanding test than any it has previously faced.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

The Politics of Cheapness: Japan’s Consumption-Tax Truce, the Yen’s Fragility and the Long Shadow of a Weaker Dollar

Japan’s cross-party push to cut the consumption tax ahead of the February 2026 election reflects the seductive politics of cheapness,...

Once an Economic Giant, Japan Now Tests a New Fiscal Path — and the World Is Watching

Global current-account imbalances widened sharply in 2024, revealing a structural divergence driven by entrenched asymmetries between surplus and deficit economies....

Why Are Electric Vehicle Loans More Expensive?

Buyers of electric vehicles face tighter financing terms compared to those who buy conventional vehicles, according to a recent paper...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment