Inflation targeting functions as a navigational star rather than a fixed rail. It anchors expectations only insofar as economic agents believe the central bank will continuously steer toward it, not merely apply the brakes once the target is breached.

Across major central banks, inflation targets remain formally symmetric, yet policy behavior increasingly suggests otherwise. In practice, 2% has come to function less as a midpoint than a ceiling. This interpretation is largely implicit and shaped by institutional constraints — most notably the effective lower bound — alongside credibility concerns and asymmetric risk perceptions. This is especially true in a post-pandemic environment marked by supply shocks and uneven disinflation.

Formally, the Federal Reserve (or Fed) continues to reaffirm a 2% longer-run inflation goal and a strategy intended to deliver 2% inflation on average over time. Credibility is often earned through revealed behavior, and recent experience has made the costs of overshooting appear more salient than the costs of sustained undershooting.

When examined comparatively, the European Central Bank (ECB) provides a clearer historical case of institutionalized asymmetry. Until its 2021 strategy review, the ECB defined price stability as inflation “below, but close to, 2%,” a formulation that created a built-in ambiguity. While seemingly cautious, the phrasing placed greater emphasis on avoiding inflation above target than on correcting persistent undershoots.

The ECB later replaced this with a symmetric 2% target in its 2021 strategy review, a change that implicitly acknowledged the credibility and communication costs of the earlier framing. This was not merely semantics: In the decade after the euro-area sovereign debt crisis, euro-area inflation outcomes repeatedly undershot the target despite substantial accommodation, contributing to concerns that expectations could settle below 2%.

Japan adds a distinct, highly current version of the same problem: Long periods of below-target inflation can change how the public and markets interpret a central bank’s reaction function. The Bank of Japan (BoJ) has maintained a clear, explicit 2% price stability target since 2013. However, the macro backdrop has recently changed: By late 2025, Japanese inflation had remained above 2% for an extended period, and public inflation expectations appeared elevated in household surveys. A Reuters report on the BoJ’s survey (based on December 2025 results) describes a large majority of households expecting prices to keep rising and notes that core inflation was still above the 2% target.

At the same time, recent coverage describes the BoJ’s policy normalization path, including policy rate increases after ending its earlier stimulus regime. The key point for the asymmetry question is whether the BoJ’s revealed tolerance bands, and the thresholds that trigger decisive action, are symmetric around 2% or more discontinuous (for example, stronger urgency when inflation risks falling back toward 0% than when inflation runs modestly above 2%). In Japan’s case, the modern record makes the downside asymmetry argument particularly plausible, because the institutional memory of deflation has been so strong.

The United Kingdom adds another angle: strong formal symmetry paired with practical judgment under uncertainty. The Bank of England’s (BoE) remit explicitly declares that the inflation target is 2% and “symmetric,” applying “at all times,” reaffirmed in the Chancellor Rachel Reeves’s monetary policy remit letter. Yet the operational challenge is that the Monetary Policy Committee must decide how much weight to place on inflation persistence versus emerging slack, and those judgments can generate time-varying asymmetry even under a symmetric mandate.

The BoE’s published Monetary Policy Summary and Minutes provides contemporaneous evidence of this balancing act. For example, the December 2025 minutes note consumer price index inflation at 3.2% (above target) while emphasizing easing pay growth and services inflation and an expected return toward target, alongside restrictive policy settings. The November 2025 minutes also show a closely split committee — 5–4 — with a minority voting for an immediate cut. This highlights that “revealed preferences” can differ across members even when the target is symmetric. In other words, the UK case shows how asymmetry can emerge from heterogeneous assessments of the inflation-output tradeoff and the risks around it.

Inflation targets derive their effectiveness not from mechanical enforcement, but from belief. When households, firms and markets trust that a central bank will actively steer inflation toward its stated objective, expectations align with that goal. When trust erodes, policy becomes less effective and more costly. This logic is well established in the academic literature, including former Fed Chair Richard Clarida and economists Jordi Galí and Mark Gertler’s foundational work on credibility and the expectations channel. The euro area’s experience after the sovereign debt crisis remains an archetypal illustration: Prolonged below-target inflation coexisted with extensive accommodation and recurring debates about whether additional easing was warranted.

Across these central banks, the common thread is that stated targets are typically simple and symmetric, while revealed reaction functions are shaped by institutional constraints (such as effective lower bounds), political economy and differing beliefs about the costs of inflation deviations. The “quiet shift” is therefore not necessarily a formal abandonment of symmetry, but an increased practical importance of thresholds, regimes and credibility repair — especially after the post-pandemic inflation shock and the uneven, category-specific price pressures that continued to affect households even during disinflation.

Progress in the aggregate

Recent inflation dynamics in the United States provide a useful contrast. Inflation decelerated steadily through 2025, with headline inflation falling from about 2.9% at the end of 2024 to roughly 2.7% by late 2025. Core inflation declined more sharply. In several categories, including gasoline and some services, prices actually fell.

From a macroeconomic perspective, this represented substantial progress toward price stability. Yet consumer sentiment remained strained. As The Wall Street Journal reported in its analysis, households remained frustrated because a slower rate of price increases did not reverse the large cumulative rise in prices since the pandemic.

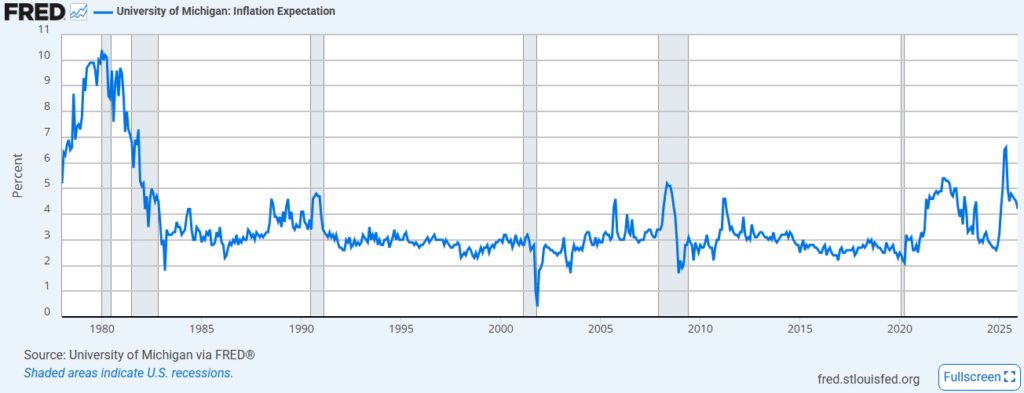

This disconnect underscores an important distinction. Inflation measures the rate of change of prices, not their level. Households care deeply about affordability, which depends on cumulative price increases relative to income growth. Even successful disinflation can leave lasting dissatisfaction if price levels remain high, a point reinforced by the University of Michigan’s consumer sentiment surveys (MICH).

This outcome does not imply a failure of US monetary policy. Inflation had already fallen dramatically from its 2022 peak, and further disinflation without significant economic damage is inherently difficult. Rather, it highlights the limits of what monetary policy can achieve once large relative price shocks have occurred.

Why consumers still felt strained

Yet improved inflation statistics did not translate into improved public sentiment. This gap reflects a fundamental distinction between inflation and affordability. Inflation measures how fast prices are changing, not how high prices already are. For many households — especially those whose wages did not keep pace with earlier price increases — everyday expenses such as groceries, rent and utilities remained significantly higher than pre-pandemic norms. Disinflation slowed the pace of deterioration but did not restore lost purchasing power.

Survey evidence reinforces this interpretation. Data from the MICH show that sentiment remained weak even as inflation moderated, indicating that households continued to feel financially constrained with their psychology.

Notably, survey responses suggest that consumers place disproportionate weight on frequently purchased necessities, particularly food, rent and energy, rather than on aggregate inflation measures. Price declines in less salient categories, therefore, did little to improve overall perceptions. This pattern is consistent with broader reporting on consumer sentiment, including an Associated Press summary noting that US consumer confidence improved modestly but remained well below pre-pandemic levels.

This divergence between macroeconomic progress and household experience highlights a crucial communication challenge. While policymakers understandably emphasize declining inflation as evidence of success, households evaluate economic conditions through the lens of price levels and income adequacy. As a result, periods of successful disinflation can still be associated with widespread dissatisfaction, even in the absence of renewed inflationary pressure.

Frameworks, forward guidance and uncertainty

The Fed’s 2020 revision of its monetary policy framework was not a routine recalibration but a response to a prolonged empirical anomaly. For nearly a decade following the Global Financial Crisis, inflation persistently undershot target despite sustained economic expansion, historically low unemployment and extraordinary monetary accommodation. Standard Phillips curve relationships appeared attenuated, wage growth remained subdued and inflation expectations drifted downward even as labor markets tightened. Against this backdrop, the revised Statement on Longer-Run Goals and Monetary Policy Strategy sought to address a credibility problem that had become structural rather than cyclical: a target that was symmetric in principle but asymmetric in outcomes.

The central innovation of the framework, often summarized as “average inflation targeting,” was less about tolerating inflation above 2% than about correcting the asymmetry embedded in prior policy practice. By conditioning future policy on realized inflation outcomes rather than on forecasts alone, the Fed aimed to counteract the persistent downside bias that had characterized inflation dynamics in the post-crisis period. In doing so, it implicitly acknowledged that credibility cannot be sustained when deviations below target are treated as benign while deviations above target provoke rapid response. The framework thus represented an attempt to restore symmetry not through mechanical rules, but through a reorientation of expectations.

This shift is especially evident in the Fed’s evolving approach to forward guidance. Minutes from the September 2020 Federal Open Market Committee meeting — released in 2025 under the Fed’s five-year disclosure rule — document a deep and explicit debate about the role of commitment under extreme uncertainty. Policymakers were operating in an environment where the conventional policy instrument had already been exhausted, the economic outlook was dominated by epidemiological rather than macroeconomic uncertainty, and the distribution of risks was sharply skewed toward catastrophic downside outcomes.

In this setting, forward guidance became the primary policy instrument, not as a signaling device about future rates per se, but as a tool for shaping expectations about the reaction function itself. Strong guidance was seen as necessary to prevent premature tightening in financial conditions and reassure households and firms that policy would remain accommodative until recovery was well advanced. The debate centered on how binding it should be — whether flexibility should be preserved at the cost of credibility, or credibility reinforced at the cost of discretion.

The eventual decision reflected a judgment that credibility losses are asymmetric and difficult to reverse. Weak or conditional guidance risked being interpreted as hedging, thereby reinforcing the perception that the inflation target functioned as a ceiling. Stronger guidance, by contrast, risked overshooting but offered a clearer focal point for expectations. In this sense, the Fed chose commitment over optionality, implicitly prioritizing expectation management over fine-tuned control.

The post-pandemic inflation surge fundamentally altered the policy environment in which this framework was implemented. Inflation rose faster and more broadly than anticipated, driven by a confluence of supply disruptions, unprecedented fiscal stimulus, shifts in consumption patterns and rapid reopening dynamics. Policymakers initially characterized these forces as transitory, a view grounded in historical experience with supply-side shocks but increasingly challenged as inflation diffused across sectors.

The subsequent tightening cycle was both rapid and forceful, marking one of the fastest increases in policy rates in modern US history. This episode is sometimes portrayed as evidence that the framework failed. A more careful interpretation is that the framework was forced to operate in a regime far removed from the one it was designed to address. The key issue was not the framework’s tolerance for above-target inflation, but the speed with which inflation exceeded any reasonable definition of “moderate.”

As Fed Chair Jerome Powell emphasized in public remarks — notably in his Jackson Hole 2025 framework review — monetary policy is not on a preset course, and Committee decisions are made based on evolving data and risk assessments rather than fixed rules. He underscored that frameworks are conditional constructs that support deliberation but do not substitute for judgment. This interpretation is reinforced by analysis of the Fed’s revised framework, which highlights how the institution adapted its strategy in response to changing economic conditions and lessons learned since the Covid-19 pandemic.

Asymmetry as an emerging norm

When the Fed’s experience is viewed alongside that of other major central banks, it becomes clear that asymmetry is a recurring feature of modern monetary regimes. The ECB’s pre-2021 formulation of price stability — explicitly asymmetric in its “below, but close to, 2%” language — provides a clear historical example. Even after adopting a symmetric target, the ECB continues to operate in an environment shaped by a decade of entrenched undershooting and weakened inflation expectations.

More broadly, the post-pandemic inflation episode has revealed a striking regularity: Central banks respond more rapidly and decisively to inflation above target than they historically did to inflation below target. This pattern is partly explained by the effective lower bound, which constrains responses to downside risks more than to upside risks. But it also reflects genuine asymmetries in policymakers’ loss functions — specifically, a greater aversion to unanchored inflation expectations than to prolonged disinflation.

Formal analysis reinforces this interpretation. Economists Michael Kiley and John Roberts illustrate that in low-rate environments, even symmetric preferences can generate asymmetric outcomes because policy space is truncated on the downside. Over time, these outcome asymmetries can become embedded in expectations, creating a self-reinforcing cycle in which private agents internalize the belief that inflation targets are ceilings rather than midpoints.

The critical issue is not whether asymmetry exists, but whether it is acknowledged and managed. When central banks insist on symmetry while systematically tolerating deviations in one direction more than the other, they weaken the informational content of the target itself. Expectations adjust not to formal statements, but to repeated patterns of behavior. Transparency about trade-offs, by contrast, can preserve credibility even in the presence of unavoidable asymmetries.

This raises deeper institutional questions: Should inflation targeting frameworks explicitly incorporate asymmetry? Or should they continue to aspire to symmetry while correcting deviations ex post? The former approach risks politicizing policy by making value judgments explicit; the latter risks eroding credibility by maintaining a rhetorical commitment that practice does not fully support.

The Japanese case

Japan offers the most sustained empirical example of how asymmetry can become institutionalized under persistent disinflation. Since the late 1990s, the Japanese economy has operated in a regime characterized by chronically low inflation, repeated encounters with the effective lower bound and deeply entrenched deflationary expectations. In this environment, asymmetry emerged as a durable feature of monetary policy design and implementation.

The policy evolution of the BoJ reflects an explicit recognition that conventional inflation-targeting symmetry was unattainable under prevailing structural conditions. The introduction of Quantitative and Qualitative Monetary Easing in 2013, followed by the adoption of Yield Curve Control (YCC) in 2016, marked a decisive shift away from short-rate management toward balance-sheet and yield-curve policies explicitly aimed at reversing deflationary psychology. These measures, paired with increasingly strong forward guidance, including state-contingent and open-ended commitments to maintain accommodation until inflation “exceeds” the target in a stable manner.

From a loss-function perspective, Japanese monetary policy became overwhelmingly asymmetric. Downside deviations from the inflation target were treated as very costly, while upside deviations were regarded as either benign or desirable. This orientation was consistent with theoretical arguments favoring history-dependent or overshooting strategies in low-inflation environments by economists GB Eggertsson and Michael Woodford and former Fed chair Ben Bernanke.

In practice, however, repeated shortfalls in realized inflation weakened the informational content of the target itself. A growing empirical literature documents how persistent outcome asymmetry reshaped expectation formation in Japan. Inflation expectations became increasingly backward-looking and adaptive, responding more strongly to realized inflation than to policy announcements or stated targets.

As forward guidance became progressively stronger but less effective, private agents rationally discounted official commitments, anchoring expectations to historical experience rather than to the central bank’s stated reaction function. In this sense, the Japanese case illustrates the limits of commitment once credibility has been eroded by prolonged underperformance.

The Japanese experience also highlights a critical distinction between commitment intensity and commitment credibility. Despite unprecedented balance-sheet expansion and explicit overshooting commitments, inflation expectations remained stubbornly below target throughout much of the pre-pandemic period. This outcome is consistent with earlier analyses emphasizing that when the effective lower bound binds repeatedly, even optimal policy may generate asymmetric results.

The post-pandemic inflation episode provided a revealing stress test of this asymmetric regime. As global inflation rose sharply in 2021–2023, Japan briefly experienced above-target inflation, driven primarily by imported cost pressures rather than domestic demand. Yet the BoJ’s response remained cautious and delayed relative to other advanced-economy central banks, reinforcing the perception that tightening is viewed as disproportionately risky given the fear of reentrenching deflation. The gradual modification and eventual exit from YCC reflected this deeply asymmetric reaction function rather than a reversion to symmetry.

From a comparative perspective, Japan complements the US and euro-area experiences by illustrating a different manifestation of the same underlying phenomenon. Asymmetry arises not only from fear of unanchored inflation expectations on the upside, but also from fear that premature tightening may reactivate deflationary dynamics. In both cases, the inflation target ceases to function as a true midpoint and instead reflects the dominant tail risk perceived by policymakers.

This broadly implies that asymmetry should be understood not as a policy error or a temporary deviation, but as an endogenous outcome of monetary regimes operating under persistent structural constraints. Japan demonstrates that once expectations internalize a one-sided reaction function, restoring symmetry becomes increasingly difficult, regardless of the formal framework in place. This reinforces a central lesson of modern monetary policy: Credibility is path-dependent, and frameworks cannot be evaluated independently of the regimes in which they are repeatedly tested.

Credibility in an uncertain world

Inflation targeting has never been merely a stabilization technology. It is fundamentally a coordination mechanism. Its effectiveness lies in its ability to align decentralized decisions — wage bargaining, price setting and investment planning — around a shared nominal anchor. That coordinating function depends critically on shared beliefs about how the central bank will respond to deviations from target, not simply on the formal statement of the objective itself.

When an inflation target is perceived as a ceiling rather than a focal midpoint, the underlying equilibrium shifts. Firms become more reluctant to raise prices, workers moderate wage demands and inflation expectations gradually drift downward. When overshoots are met with swift and forceful policy responses while undershoots are tolerated for extended periods, symmetry exists largely in rhetoric: The target ceases to anchor expectations and instead defines a one-sided constraint.

The experience of the past decade suggests that symmetry cannot be assumed. It must be continuously produced through consistent action, credible communication and institutional arrangements that reinforce the central bank’s willingness to respond to deviations in both directions. In an environment characterized by recurrent supply shocks, geopolitical fragmentation, climate-related disruptions and increasingly complex fiscal-monetary interactions, maintaining that symmetry has become structurally more difficult.

Asymmetric inflation targeting should therefore be understood not primarily as a doctrinal choice, but as an emergent property of modern monetary regimes operating under binding constraints. The challenge for policymakers is not to deny this reality, but to confront it explicitly: to distinguish between asymmetry as a necessary adaptation to tail risks and asymmetry that, over time, erodes the informational content of the target itself.

Vitally, the post-pandemic period complicates how symmetry is assessed. Central banks have both undershot and overshot inflation targets over the past decade, with the most visible overshoot occurring during the Covid-19 shock and its aftermath. That episode did not create the underlying asymmetry; it temporarily overlaid a large positive inflation shock on frameworks that had already displayed persistent one-sided tendencies before 2020. In doing so, the overshoot mechanically pulled multi-year inflation averages closer to target, making outcomes appear more balanced than the underlying reaction function may be.

The open question is whether central banks now revert to pre-pandemic asymmetry as inflation approaches target, or whether the experience of the effective lower bound and the political costs of inflation have produced a more cautious — and potentially different — policy equilibrium.

Failing to draw that distinction risks undermining the very expectations that give monetary policy its leverage. A nominal anchor that restrains drift in only one direction eventually becomes less an anchor than a tide marker, recording deviations after they occur rather than preventing them.

[Lee Thompson-Kolar edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

Europe’s Return to the Deflation Trap

Europe drifts back toward a low-inflation equilibrium as institutional inertia, weak fiscal capacity and persistent demand shortfalls reemerge across the...

Abe and Kishida: The Two Contrasting Visions for Japan’s Political Economy

Japan’s recent economic history is defined by two contrasting visions: Shinzo Abe’s bold reflationary drive centered on monetary innovation and...

Bridging the Divide: Inflation Expectations, Consumer Sentiment and the Fed’s Challenge

Despite slowing inflation rates, consumers remain concerned about high prices due to cumulative cost increases since the Covid-19 pandemic. This...

Central Bank Independence Is Unbelievably Valuable for the World Economy

To ensure sound monetary policy and economic stability, central banks like the US Federal Reserve need their independence (CBI). Opposing...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Comment