Every January, inflation seems to wake up before the rest of the economy. Recent reporting in the Wall Street Journal (WSJ) suggests that prices are heating up again, markets are twitching and analysts are searching for culprits — from tariffs to corporate pricing power. But sometimes the drama says more about the calendar than about the economy itself.

The idea of “residual seasonality” — the lingering seasonal bias that survives even after statistical adjustments — has become a powerful lens through which to interpret recent inflation data. Research from Federal Reserve economists suggests that residual seasonality may help explain why January inflation often appears elevated — though interpretations of what this means for policy remain open to debate.

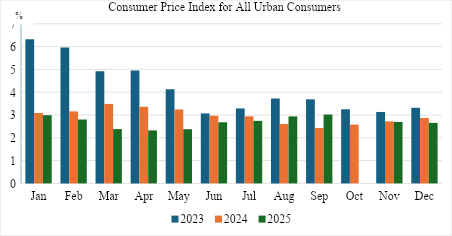

Yet the most recent data introduce a subtle twist. January 2026 inflation came in at roughly 2.4% (2.39%), noticeably cooler than the elevated early-year averages seen during 2023–2025. Rather than contradicting the idea of residual seasonality, this softer reading complicates it. If previous January spikes reflected a mixture of pricing resets, tariff effects and statistical noise, the latest number suggests that the seasonal “heat” is not guaranteed to repeat. The illusion, it seems, fades when underlying inflation momentum weakens enough.

A seasonal curve and a shift in momentum

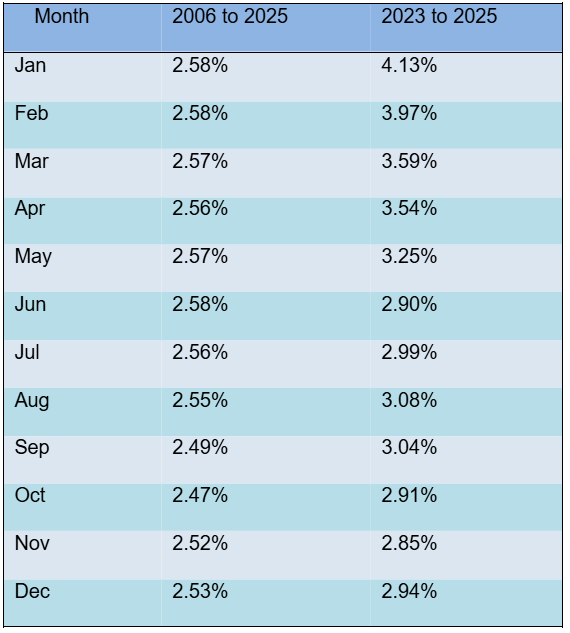

Consider the longer historical pattern. From 2006 to 2025, average monthly inflation has been remarkably stable, hovering around the mid-2% range: roughly 2.58% in January, 2.57% in March and 2.47% in October. The seasonal curve is gentle, almost flat — a quiet baseline that rarely attracts attention. Yet when we isolate the more recent period from 2023 to 2025, the curve shifts upward. January jumps to 4.13%, February to 3.97% and March to 3.59%. By late summer and autumn, the numbers cool toward the low-3% range, with October at 2.91% and November near 2.85%.

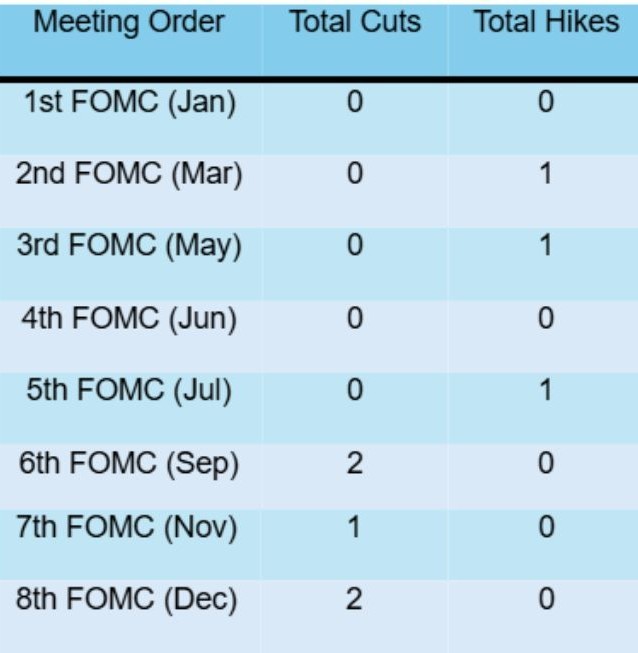

The image of a tide offers a useful way to think about monetary policy, because central banks rarely react to every passing wave. Policymakers do not chase each crest of incoming data; instead, they try to read the direction of the current beneath the surface. Between 2023 and 2025, the Federal Reserve’s actions appeared less tied to isolated monthly fluctuations and more aligned with the broader trajectory of disinflation. Rate hikes were concentrated earlier in the year in 2025 — with single increases in February, March, May and July — at a time when inflation remained elevated relative to its longer-term trend.

As the year progressed and price pressures gradually eased, the policy stance shifted. Cuts emerged later, with two reductions in September and December and additional moves in October and November, coinciding with inflation readings that had moved closer to historical norms.

Taken together, this sequence suggests that policymakers were responding to underlying momentum rather than short-term noise. If a strong January inflation print resembles a dramatic opening note in a symphony, the Federal Reserve appears more concerned with the evolving melody than with the volume of any single instrument.

The softer inflation reading in January 2026 reinforces this interpretation. Rather than reigniting fears of renewed tightening, the cooler data point implies that patience during the disinflation process may have allowed seasonal distortions to dissipate naturally, enabling policymakers to maintain a steadier course as the economic tide gradually turned.

Tariffs, corporate strategy and the fading distortion

The debate over tariffs adds another layer to the narrative. Some observers argue that higher import duties have encouraged companies to push up prices at the start of the year. But tariffs and seasonal pricing habits often move together, making it difficult to isolate cause and effect. Businesses frequently reset prices in January — adjusting service fees, subscription plans or post-holiday discounts — regardless of trade policy. In that sense, tariffs may act less like the engine of inflation and more like a gust of wind that amplifies a seasonal pattern already in motion. The fact that January 2026 inflation cooled despite these dynamics suggests that structural demand conditions may now matter more than seasonal timing.

Corporate behavior hints at this complexity. As consumers became more cautious after years of rising prices, companies began experimenting with affordability strategies: smaller packaging, promotional discounts or diversified price tiers. These shifts suggest that demand conditions are evolving alongside cost pressures. When shoppers hesitate, businesses may find it harder to sustain aggressive price increases — a dynamic consistent with the recent return to lower inflation levels.

Residual seasonality, then, is less a technical curiosity than a reminder of how economic data can mislead. Imagine looking at the economy through a window with faint vertical lines etched into the glass. You can still see the landscape beyond, but certain shapes appear distorted depending on the angle of light. January inflation may be one of those distortions — but the cooler 2026 reading shows that the distortion itself can fade when underlying conditions change.

The long horizon beyond the January illusion

What makes the recent period particularly revealing is how policy actions align with the seasonal curve. The early-year months that saw rate hikes also carried inflation averages well above the historical baseline, while the months with cuts coincided with cooling readings. This alignment suggests that policymakers were responding to persistent trends rather than reacting reflexively to single data releases. The softer start to 2026 further supports this interpretation: rather than chasing a seasonal spike, policy appears to be anchored to the broader inflation trajectory.

For readers following the story, the temptation is to treat each inflation report like a weather alert. A hotter-than-expected January feels like a thunderclap, a signal that the storm has returned. But the broader statistics tell a quieter story: a gradual shift from elevated inflation toward something closer to normal. And when January itself cools — as it did in 2026 — it reminds us that even familiar seasonal narratives can lose their grip when the economic climate changes.

In many ways, inflation behaves like a marathon runner at the start of a race. The opening pace may look fast, even frantic, but the real story emerges only over distance. Policymakers appear to recognize this dynamic, adjusting interest rates only when the runner’s rhythm changes consistently rather than when a single split time surprises observers.

And perhaps that is the most important lesson hidden inside the January illusion. Like a mirage on a desert road, a sudden burst of heat can capture attention and distort perception. But step back far enough — and include the cooler reading of January 2026 — and the landscape resolves into something steadier: a long horizon where seasons change slowly, tides rise and fall predictably, and the economy moves forward not in sudden jolts but in measured, deliberate rhythms.

[Kaitlyn Diana edited this piece.]

The views expressed in this article are the author’s own and do not necessarily reflect Fair Observer’s editorial policy.

When Inflation Targets Become Ceilings

Across major central banks, inflation targets remain formally symmetric, yet policy behavior increasingly reveals asymmetry. Prolonged undershooting, effective lower bounds...

Bridging the Divide: Inflation Expectations, Consumer Sentiment and the Fed’s Challenge

Despite slowing inflation rates, consumers remain concerned about high prices due to cumulative cost increases since the Covid-19 pandemic. This...

The Fed and Inflation: What’s Next?

With inflation remaining stubbornly above the Federal Reserve’s 2% target, policymakers must navigate a complex landscape of economic pressures. While...

Support Fair Observer

We rely on your support for our independence, diversity and quality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 3,000+ voices from 90+ countries. We also conduct education and training programs

on subjects ranging from digital media and journalism to writing and critical thinking. This

doesn’t come cheap. Servers, editors, trainers and web developers cost

money.

Please consider supporting us on a regular basis as a recurring donor or a

sustaining member.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.

Is the German Economy Now Destined to Decline?

The German economy is in crisis and its much-vaunted economic model is in question. The Russia–Ukraine War, a contracting Chinese...

Comment